Key Takeaways

-

Small adjustments to your retirement strategy can significantly boost your savings and financial security in 2025.

-

Federal employees have unique opportunities and benefits to maximize retirement savings with careful planning.

Understanding the Importance of Fine-Tuning Your Retirement Plan

- Also Read: How-to Compare Inflation Protection Strategies for Federal Retirees in 2026

- Also Read: Health Expense Budgeting: 8 Tips for Retirees Planning Medical Costs

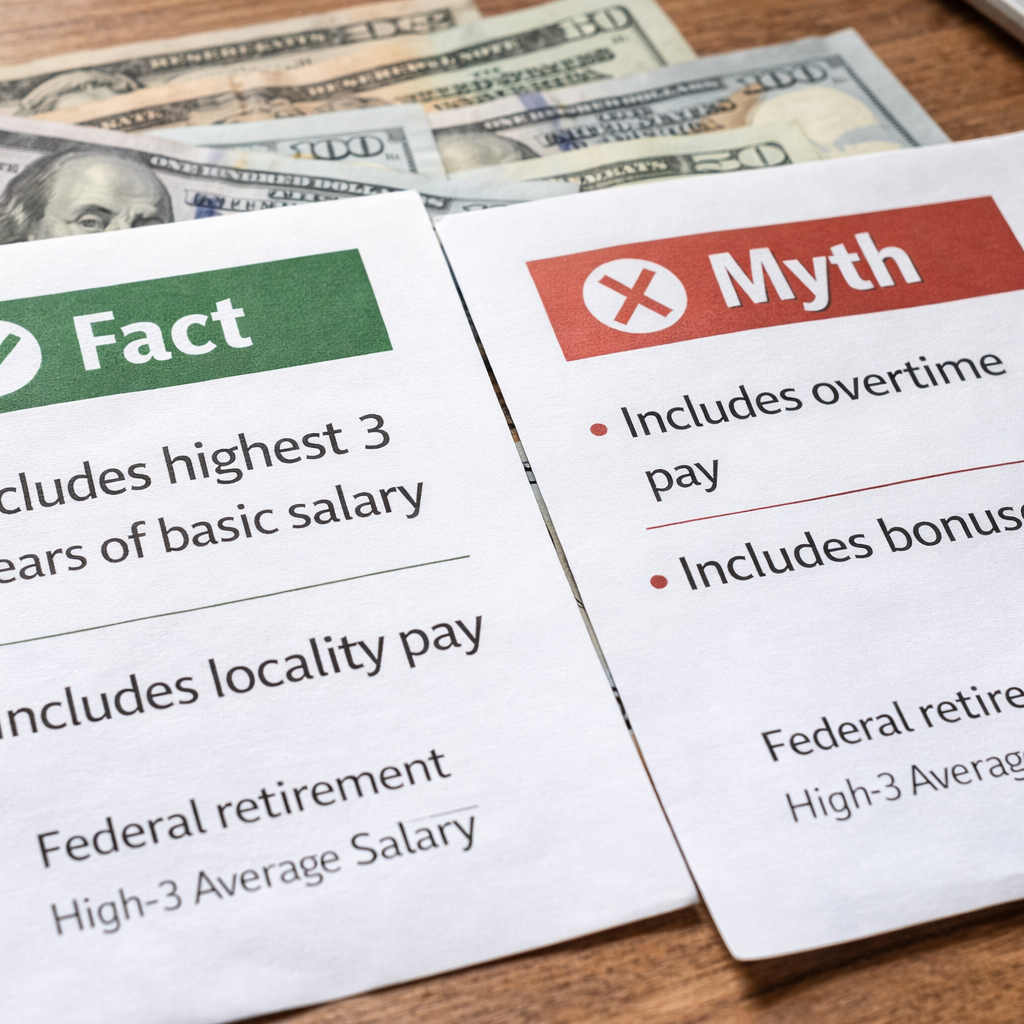

- Also Read: High-3 Average Salary Explained: Myths vs Facts for Federal Retirement

1. Reassessing Contributions to Your Thrift Savings Plan (TSP)

The Thrift Savings Plan (TSP) is a cornerstone of federal retirement savings. For 2025, the elective deferral limit is $23,500, with additional catch-up contributions of up to $7,500 if you’re aged 50 or older. Adjusting your contributions to hit these limits can significantly boost your nest egg. Consistently increasing your contributions over time is one of the simplest ways to enhance your financial security.

Why It Matters:

The TSP offers government matching contributions and low administrative fees, making it one of the most cost-effective ways to save. The sooner you contribute the maximum allowed, the longer your investments have to grow, thanks to compounding.

Action Steps:

-

Review your current contribution levels and determine if you’re maximizing the government match.

-

Set a goal to increase contributions gradually if you’re not already maxing out.

-

If you’re 60-63, consider the special catch-up provision that allows even higher contributions during this period.

-

Adjust your payroll deductions through your agency’s HR system or portal to ensure you reach your target.

2. Fine-Tuning Your Investment Allocations

Your TSP investments play a critical role in growing your retirement savings. In 2025, ensuring that your investment choices align with your risk tolerance and retirement timeline is essential. Market fluctuations can significantly impact your savings if your portfolio isn’t appropriately balanced.

Why It Matters:

Market conditions and personal circumstances change over time. Keeping an eye on your allocations can help protect your savings from unnecessary risks while still allowing for growth. A diversified portfolio reduces exposure to volatile markets while improving the likelihood of steady returns.

Action Steps:

-

Check your current allocations among the TSP funds (G, F, C, S, and I funds) to ensure proper diversification.

-

If you prefer a hands-off approach, consider lifecycle funds, which automatically adjust based on your target retirement date.

-

Rebalance your portfolio annually or whenever your goals or market conditions shift.

-

Monitor market trends to determine if adjustments to asset classes are necessary for better returns.

3. Reviewing Your Federal Employees Health Benefits (FEHB) and Medicare Options

Health insurance is a significant part of retirement planning. In 2025, FEHB premiums have risen, and integrating your benefits with Medicare could save you money. As healthcare needs evolve, your chosen plan should reflect the level of care you expect to need in the coming years.

Why It Matters:

Healthcare costs are often underestimated in retirement. Ensuring you have comprehensive coverage while minimizing costs can preserve more of your savings. Aligning your FEHB with Medicare could help lower premiums, reduce deductibles, and provide additional financial relief.

Action Steps:

-

Review your FEHB plan during Open Season (November 11 to December 13) to find options with the best coverage for your needs.

-

If eligible for Medicare, explore how combining it with your FEHB plan can reduce out-of-pocket expenses.

-

Factor future healthcare needs, such as prescription drugs and specialist visits, into your coverage decisions.

-

Take advantage of FEHB plans offering additional benefits for enrollees who also have Medicare.

4. Exploring the Benefits of Catch-Up Contributions

If you’re 50 or older, catch-up contributions offer a unique opportunity to accelerate your savings. In addition to the TSP, consider increasing contributions to other retirement accounts, such as IRAs, for a more diversified retirement portfolio.

Why It Matters:

These extra contributions allow you to make up for earlier years when saving might have been more challenging. They also provide significant tax advantages. As you near retirement, these additional savings can bridge gaps in your long-term financial plan.

Action Steps:

-

Allocate any extra income or bonuses toward catch-up contributions.

-

Evaluate whether you’re fully utilizing other retirement accounts, such as Roth or traditional IRAs.

-

Use employer-provided tools or calculators to project how these contributions will impact your total savings.

-

Monitor your progress regularly to ensure you’re on track to meet your goals.

5. Evaluating Your Federal Pension Options

Your federal pension is a critical component of your retirement income. Understanding your options for maximizing it can significantly impact your financial future. The decisions you make now about your pension will shape your retirement income for decades.

Why It Matters:

Federal pensions, especially under the FERS system, provide a stable source of income. Decisions about survivor benefits, retirement dates, and service credit purchases can alter your benefits. Planning ahead ensures that you maximize your annuity without compromising other aspects of your financial plan.

Action Steps:

-

Determine your High-3 average salary and how it affects your annuity calculation.

-

Decide whether to opt for a survivor benefit for your spouse or dependents.

-

If applicable, look into buying back military service time to increase your annuity.

-

Review your retirement timeline to determine the best time to retire based on your service years and age.

6. Creating a Withdrawal Strategy for Retirement Income

A well-planned withdrawal strategy ensures that you can maintain your standard of living without outliving your savings. Federal retirees must carefully balance withdrawals from TSP, Social Security, and pensions to optimize their income streams.

Why It Matters:

Drawing from your accounts in the right order can minimize taxes and maximize the longevity of your savings. Coordinating income streams helps avoid financial gaps and ensures you meet RMD requirements.

Action Steps:

-

Plan to withdraw from taxable accounts first to allow tax-advantaged accounts to grow longer.

-

Factor in Required Minimum Distributions (RMDs) starting at age 73 and adjust your withdrawals accordingly.

-

Work with a financial advisor to create a tax-efficient withdrawal strategy tailored to your needs.

-

Regularly monitor your withdrawal rates to ensure you’re staying within sustainable limits.

Embracing Long-Term Success with Periodic Reviews

Retirement planning isn’t static. Regularly reviewing your financial situation and adjusting your strategy ensures that your plan stays aligned with your evolving needs and goals. For federal employees, the benefits you’ve earned are valuable tools—but they must be actively managed to yield the best results.

What You Should Do Now:

-

Schedule an annual review of your retirement plan.

-

Stay informed about changes to federal benefits and adjust accordingly.

-

Take advantage of resources, such as financial planning services, offered through your agency or retirement programs.

-

Remain proactive by setting clear goals for the coming years.

Secure Your Retirement Future in 2025 and Beyond

Taking control of your retirement planning by making these six adjustments can improve your financial security and peace of mind. Whether it’s optimizing your TSP contributions, reviewing your health benefits, or rebalancing your investments, small changes today can make a big difference tomorrow. Stay proactive, informed, and committed to your financial well-being.