Advertisement

Federal Employees Retirement System (FERS)

The Federal Employees Retirement System (FERS) is the foundation of retirement security for millions of federal employees. Established in 1987, FERS was designed to replace the outdated Civil Service Retirement System (CSRS) and to provide federal workers with a modern, flexible, and comprehensive retirement plan. As of 2024, FERS remains the primary retirement system for nearly 98% of the federal workforce, covering a broad spectrum of employees ranging from civilian workers to uniformed services personnel. We will look into the intricate details of FERS, exploring its three primary components, recent updates, strategies for maximizing benefits, and essential planning tips to ensure a secure and comfortable retirement.

The Importance of FERS in Retirement Planning

Retirement planning is a critical aspect of financial management, particularly for federal employees who rely on the Federal Employees Retirement System (FERS) for their post-employment income. FERS is not just a pension plan; it is a multifaceted system designed to provide federal employees with financial stability through a combination of pension, Social Security benefits, and investment opportunities. Understanding the components of FERS and how they work together is crucial for federal employees at all stages of their careers, from new hires to those nearing retirement. By understanding FERS, employees can make informed decisions that maximize their retirement benefits and provide peace of mind during their golden years.

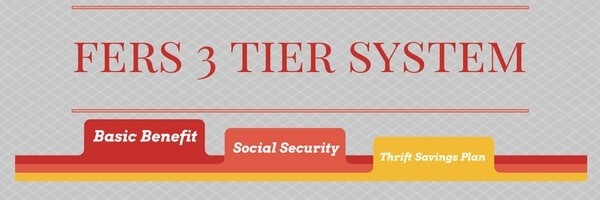

The Three-Tiered Structure of FERS

FERS is designed as a three-tiered system, each component playing a vital role in providing a comprehensive retirement package:

- FERS Basic Benefit Plan: This is a defined benefit plan, which means it provides a guaranteed monthly pension upon retirement. The amount of this pension is based on the employee’s years of service and the average of their highest three years of salary, commonly referred to as the “high-3.” The Basic Benefit Plan is the backbone of the FERS system, ensuring a steady stream of income throughout retirement.

- Social Security Benefits: Under FERS, federal employees contribute to Social Security throughout their careers, similar to private-sector workers. These contributions make them eligible to receive Social Security benefits upon reaching retirement age, adding an additional layer of financial security. The integration of Social Security into FERS is one of the key differences between FERS and its predecessor, CSRS.

- Thrift Savings Plan (TSP): The TSP is a defined contribution plan similar to a 401(k), offering employees the opportunity to save and invest a portion of their income. The federal government matches employee contributions up to 5%, making it an essential component of the retirement planning strategy. The TSP offers a variety of investment options, allowing employees to tailor their portfolios based on their risk tolerance and retirement goals.

Together, these three components create a robust and flexible retirement system that meets the diverse needs of federal employees.

Advertisement

FERS Basic Benefit Plan: The Core of Your Retirement Income

The FERS Basic Benefit Plan is the cornerstone of your retirement income. As a defined benefit plan, it provides a predictable and stable monthly payment based on your years of service and salary history. The plan is funded through employee contributions and government matching, ensuring that it remains a reliable source of income throughout your retirement.

Calculation of the FERS Pension:

The pension amount under the FERS Basic Benefit Plan is calculated using a formula that takes into account your years of service and your high-3 average salary. The formula is as follows:

- For those retiring before age 62 or with less than 20 years of service: 1% of your high-3 average salary multiplied by your years of creditable service.

- For those retiring at age 62 or older with 20 or more years of service: 1.1% of your high-3 average salary multiplied by your years of creditable service.

For example, if you retire at age 62 with 30 years of service and a high-3 average salary of $100,000, your annual pension would be:

100,000 x 1.1% x 30 = $33,000

This pension is paid out monthly for life and is subject to Cost of Living Adjustments (COLA), which help to maintain your purchasing power in the face of inflation. The FERS Basic Benefit Plan is particularly valuable because it provides a guaranteed income stream that is not subject to market fluctuations, making it a stable foundation for your retirement

Cost of Living Adjustments (COLA):

COLA adjustments are a vital feature of the FERS Basic Benefit Plan, helping to preserve the purchasing power of your pension over time. In 2024, the COLA for FERS retirees is set at 2.2%. This adjustment, while modest, is crucial in an economic environment where inflation can erode the value of fixed incomes. COLA adjustments are typically based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), ensuring that your pension keeps pace with rising costs of living.

Social Security Benefits Under FERS

A significant advantage of FERS over the older CSRS system is the inclusion of Social Security benefits. As a FERS employee, you contribute to Social Security via payroll taxes, just like other American workers. These contributions make you eligible to receive Social Security benefits upon retirement, adding an additional layer of financial security.

Eligibility and Benefit Calculation:

Social Security benefits under FERS are calculated based on your highest 35 years of earnings. The benefit amount is determined by your average indexed monthly earnings (AIME) and the age at which you begin receiving benefits. You can start receiving benefits as early as age 62, but doing so will reduce your monthly payment. Waiting until full retirement age (66 or 67, depending on your birth year) allows you to receive full benefits, with an increase if you delay claiming until age 70.

The integration of Social Security into FERS provides a significant advantage, offering federal employees a diversified retirement income stream that includes both a pension and Social Security. This dual-income approach helps to mitigate the risks associated with relying on a single source of retirement income.

Impact of the Windfall Elimination Provision (WEP) and Government Pension Offset (GPO):

For federal employees who have service under the older CSRS system, the Windfall Elimination Provision (WEP) and Government Pension Offset (GPO) are critical considerations. The WEP can reduce your Social Security benefits if you receive a pension from work not covered by Social Security (such as CSRS). Similarly, the GPO can reduce Social Security spousal or survivor benefits if you receive a government pension from work not covered by Social Security. These provisions are complex and can significantly impact your retirement income, making it essential to understand how they apply to your situation.

Thrift Savings Plan (TSP): Building Your Investment Portfolio

The Thrift Savings Plan (TSP) is a powerful tool in your retirement planning arsenal. It functions similarly to a 401(k), allowing you to save and invest a portion of your income with the benefit of employer matching. The TSP is particularly valuable because it offers low fees and a range of investment options, making it an efficient and flexible way to build your retirement savings.

Key Features of the TSP:

- Contribution Limits: The TSP has generous contribution limits, allowing you to save up to $23,000 per year in 2024, with an additional $7,500 catch-up contribution allowed for employees aged 50 and over. These high contribution limits enable you to maximize your retirement savings, particularly in the years leading up to retirement.

- Investment Options: The TSP offers a variety of investment funds, ranging from conservative government securities (G Fund) to more aggressive options like the Common Stock Index Investment Fund (C Fund). Each fund has its own risk and return profile, allowing you to tailor your investment strategy to your risk tolerance and retirement timeline. The TSP also offers Lifecycle Funds, which automatically adjust your investment mix as you approach retirement, providing a hands-off investment option for those who prefer a more passive approach.

- Employer Matching: One of the most significant benefits of the TSP is the federal government’s matching contribution. The government matches your contributions up to 5% of your salary, making it essential to contribute at least that amount to take full advantage of this benefit. This matching contribution is essentially free money and can significantly boost your retirement savings over time.

Withdrawal Options: Upon retirement, you have several options for withdrawing your TSP funds. These options include:

- Lump-Sum Payment: You can choose to receive your entire TSP balance in one lump-sum payment. This option provides immediate access to your funds but also comes with significant tax implications, as the entire amount will be subject to income tax in the year of withdrawal.

- Monthly Payments: You can set up regular withdrawals from your TSP account, receiving a steady stream of income throughout your retirement. Monthly payments can be based on a fixed amount or calculated based on your life expectancy.

- Annuity Purchase: You can convert your TSP balance into a lifetime annuity, which provides guaranteed income for the rest of your life. This option offers the security of knowing that you will not outlive your retirement savings, but it also comes with trade-offs, such as losing access to the principal balance.

Each withdrawal option has different tax implications and risks, so it’s crucial to consult with a financial advisor to determine the best strategy for your situation.

Recent FERS Updates in 2024: What You Need to Know

The Federal Employees Retirement System has undergone several updates in 2024 that affect both current employees and retirees. Staying informed about these changes is essential for effective retirement planning:

- Cost of Living Adjustments (COLA): The COLA for FERS retirees in 2024 is set at 2.2%. This adjustment, though modest compared to the previous year’s COLA, is critical for helping retirees maintain their purchasing power in the face of rising costs. COLA adjustments are typically based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). For 2024, the adjustment helps offset inflationary pressures, particularly in essential areas like healthcare and housing.

- TSP Contribution Limits: The IRS has increased the TSP contribution limits to $23,000 for 2024, with an additional $7,500 catch-up contribution allowed for employees aged 50 and over. These higher limits provide federal employees with more opportunities to save for retirement, especially as they approach the end of their careers. Maximizing contributions during the peak earning years can significantly enhance retirement savings, providing greater financial security in retirement.

- Locality Pay Adjustments: Locality pay adjustments have also been updated for 2024, which may impact your high-3 salary calculation. These adjustments are crucial for those nearing retirement, as the high-3 salary is used to calculate your FERS pension. Ensuring that you accurately understand how these adjustments affect your salary and pension can help you make more informed retirement planning decisions.

- Phased Retirement: The phased retirement program has been expanded, allowing more federal employees to reduce their working hours while beginning to draw on their retirement benefits. This option is particularly beneficial for those who want to ease into retirement gradually, maintaining a part-time income while transitioning to full retirement. Phased retirement can also provide valuable time to adjust your financial plans as you move from full-time employment to retirement.

These updates highlight the importance of staying informed and adapting your retirement planning strategies as policies evolve. Being aware of these changes allows you to make the most of your FERS benefits and ensures that you are well-prepared for retirement.

Strategic Retirement Planning Under FERS

Planning for retirement under FERS requires a strategic approach, taking into account the various components of the system and how they interact. Here are some key strategies to help you maximize your FERS benefits and achieve a secure retirement:

- Start Saving Early: The earlier you begin contributing to your TSP, the more you benefit from compound interest. Even small contributions made early in your career can grow substantially over time. Aim to contribute at least 5% of your salary to take full advantage of the government matching contributions. If you can, try to max out your contributions each year, especially as you approach retirement age.

- Regularly Review Your Retirement Plan: Life circumstances and financial markets change, and so should your retirement plan. Regularly reviewing your FERS benefits, TSP investments, and Social Security strategy ensures that your plan remains aligned with your retirement goals. Tools like the Federal Ballpark Estimator can help you with your retirement income and make necessary adjustments.

- Optimize Your Social Security Benefits: Deciding when to start receiving Social Security benefits is a critical decision in retirement planning. While you can begin benefits at age 62, waiting until full retirement age or later increases your monthly payments. Consider factors such as your health, financial needs, and retirement goals when deciding the best time to start your Social Security benefits.

- Understand the Interaction Between FERS and Social Security: If you have service under both CSRS and FERS, or if you are eligible for Social Security spousal or survivor benefits, it’s important to understand how the Windfall Elimination Provision (WEP) and Government Pension Offset (GPO) might affect your benefits. These provisions can reduce your Social Security benefits, so understanding their impact is crucial for accurate retirement planning.

- Seek Professional Guidance: Retirement planning, especially under FERS, can be complex. Consulting with a financial advisor who specializes in federal employee benefits can help you navigate the intricacies of the system and develop a comprehensive retirement strategy. An advisor can provide personalized advice on topics such as TSP investment choices, Social Security timing, and pension optimization, helping you make informed decisions that maximize your retirement benefits.

Understanding the Complexities of FERS and Social Security

For federal employees, particularly those who have service under the CSRS system or are eligible for Social Security spousal or survivor benefits, the interaction between FERS and Social Security can be complex. Two provisions, in particular, can significantly impact your retirement income: the Windfall Elimination Provision (WEP) and the Government Pension Offset (GPO).

- Windfall Elimination Provision (WEP): The WEP can reduce your Social Security benefits if you receive a pension from work not covered by Social Security, such as service under the CSRS system. The WEP formula reduces the amount of your Social Security benefit, but the reduction is capped, ensuring that it does not completely eliminate your benefit. The impact of the WEP depends on your years of substantial earnings under Social Security and your total years of service.

- Government Pension Offset (GPO): The GPO affects Social Security spousal and survivor benefits if you receive a government pension from work not covered by Social Security. The GPO reduces your Social Security benefit by two-thirds of your government pension. This reduction can significantly impact the amount of spousal or survivor benefits you receive, making it essential to understand how the GPO applies to your situation.

Understanding how these provisions interact with your FERS benefits is crucial for accurate retirement planning. If you are affected by the WEP or GPO, it’s important to plan accordingly, considering the potential reductions in your Social Security benefits when estimating your total retirement income.

- Seek Professional Guidance: Retirement planning, especially under FERS, can be complex. Consulting with a financial advisor who specializes in federal employee benefits can help you navigate the intricacies of the system and develop a comprehensive retirement strategy. An advisor can provide personalized advice on topics such as TSP investment choices, Social Security timing, and pension optimization, helping you make informed decisions that maximize your retirement benefits.

Maximizing Your Thrift Savings Plan (TSP): Investment Strategies

The Thrift Savings Plan (TSP) is a powerful tool for federal employees, offering a range of investment options and the benefit of employer matching. However, to maximize your TSP, it’s essential to develop a sound investment strategy that aligns with your retirement goals and risk tolerance.

Diversifying Your Investments:

The TSP offers a variety of funds, each with different risk and return profiles. Diversifying your investments across these funds can help manage risk while providing opportunities for growth. The TSP funds include:

- G Fund: Government Securities Investment Fund, which invests in short-term U.S. Treasury securities. It offers stability and low risk, but with lower returns.

- F Fund: Fixed Income Index Investment Fund, which tracks the Bloomberg Barclays U.S. Aggregate Bond Index. It provides moderate risk and return, with income from interest on bonds.

- C Fund: Common Stock Index Investment Fund, which tracks the S&P 500 Index. It offers higher risk and return, with potential for significant growth.

- S Fund: Small Capitalization Stock Index Investment Fund, which tracks the Dow Jones U.S. Completion TSM Index. It offers high risk and return, focusing on small and mid-sized U.S. companies.

- I Fund: International Stock Index Investment Fund, which tracks the MSCI EAFE Index. It provides exposure to international markets, with high risk and return.

- L Funds: Lifecycle Funds, which automatically adjust your investment mix as you approach your retirement target date. These funds offer a hands-off approach to investing, gradually reducing risk as you near retirement.

Contribution Strategies:

Maximizing your contributions to the TSP is critical for building a strong retirement portfolio. Aim to contribute at least 5% of your salary to take full advantage of the government matching contributions. If possible, try to max out your contributions each year, especially as you approach retirement age. The TSP’s low fees make it an efficient way to save for retirement, and the power of compound interest can significantly increase your savings over time.

Withdrawal Planning:

Planning for withdrawals from your TSP is just as important as contributing to it. Upon retirement, you have several options for accessing your TSP funds, each with different tax implications and risks. It’s essential to understand these options and choose the one that best aligns with your retirement income needs:

- Lump-Sum Withdrawal: This option provides immediate access to your funds, but the entire amount is subject to income tax in the year of withdrawal. It’s a risky option if you’re not disciplined with spending or if you face a large tax bill.

- Periodic Payments: You can set up regular withdrawals from your TSP, providing a steady income stream. This option allows for more control over your tax liability and ensures that your funds last throughout retirement.

- Annuity Purchase: Converting your TSP balance into an annuity provides guaranteed income for life, offering peace of mind that you won’t outlive your savings. However, it also means giving up access to the principal balance, which may not be ideal if you need flexibility in your retirement income.

Consulting with a financial advisor can help you develop a withdrawal strategy that balances your need for income with the desire to minimize taxes and preserve your savings.

The Benefits of Phased Retirement

Phased retirement is an option that allows federal employees to transition into retirement gradually by reducing their working hours while beginning to draw on their retirement benefits. This program is particularly beneficial for those who are not yet ready to fully retire but want to start enjoying some of the benefits of retirement.

Advantages of Phased Retirement:

- Income Continuation: Phased retirement allows you to maintain a steady income while reducing your work hours. This can be particularly beneficial if you’re not yet ready to rely solely on your retirement savings.

- Social Security Benefits: By continuing to work part-time, you can delay claiming Social Security benefits, which increases your monthly benefit when you eventually start receiving it gradually. This can result in higher lifetime benefits and provide more financial security as you transition into full retirement.

- Retirement Planning Flexibility: Phased retirement provides extra time to plan and adjust your retirement strategy. You can use this time to fine-tune your investment portfolio, reassess your retirement income needs, and ensure that your plans align with your goals.

- Health Insurance Continuation: During phased retirement, you can continue to receive health insurance benefits, which is a significant advantage for those not yet eligible for Medicare. This ensures that you maintain essential healthcare coverage while working reduced hours.

Under the phased retirement program, employees work part-time while receiving a portion of their FERS pension. This arrangement allows employees to continue earning income while easing into retirement. It also provides additional time to adjust to the financial and lifestyle changes that come with retirement.

Considerations for Phased Retirement:

While phased retirement offers many benefits, it’s essential to consider the potential downsides. Working part-time may not provide the same level of income as full-time employment, which could impact your ability to save for retirement. Additionally, phased retirement requires careful coordination with your employer and understanding of how your pension and benefits will be affected.

If you’re considering phased retirement, it’s advisable to consult with a financial advisor who can help you navigate the complexities of the program and develop a strategy that meets your needs.

Preparing for Retirement: Practical Steps to Take

Preparing for retirement under FERS involves several practical steps to ensure that you maximize your benefits and achieve financial security. Here are some key actions to take as you approach retirement:

- Understand Your Benefits: Take the time to fully understand your FERS benefits, including your pension, TSP, and Social Security. Use online tools like the Federal Ballpark Estimator to get a clear picture of your retirement income and how it will support your post-retirement lifestyle.

- Create a Retirement Budget: Developing a detailed retirement budget is essential for managing your finances during retirement. Consider your expected income from FERS, TSP withdrawals, and Social Security, and compare it to your anticipated expenses. This will help you determine if your savings are sufficient or if adjustments are needed.

- Plan for Healthcare Costs: Healthcare is a significant expense in retirement, and it’s important to plan for these costs. Consider how you will cover healthcare expenses, including the costs of Medicare, supplemental insurance, and out-of-pocket expenses. Ensure that your retirement plan accounts for these potential costs.

- Evaluate Your TSP Withdrawal Strategy: As you approach retirement, review your TSP withdrawal options and decide on a strategy that best fits your income needs. Consider the tax implications of different withdrawal options and how they align with your overall retirement plan.

- Consult with a Financial Advisor: Retirement planning under FERS can be complex, and it’s wise to seek professional guidance. A financial advisor with experience in federal benefits can help you navigate the various options and develop a comprehensive retirement strategy that aligns with your goals.

- Consider Estate Planning: Estate planning is an important aspect of retirement preparation. Ensure that your will, beneficiary designations, and other estate planning documents are up to date. Consider how you want your assets distributed and whether you need to take steps to minimize estate taxes.

- Review Your Insurance Needs: As you approach retirement, review your life insurance and other insurance needs. Determine if your current coverage is sufficient or if adjustments are necessary to protect your financial security in retirement.

By taking these steps, you can ensure that you are well-prepared for retirement and that your financial plan supports your desired lifestyle.

Securing Your Future with FERS

The Federal Employees Retirement System (FERS) offers a comprehensive and robust retirement plan that provides federal employees with the tools they need to achieve financial security in retirement. However, maximizing the benefits of FERS requires careful planning, a thorough understanding of the system, and proactive management of your retirement strategy.

With the updates to FERS in 2024, it’s more important than ever for federal employees to stay informed and take advantage of the resources available to them. By understanding the components of FERS, optimizing your Thrift Savings Plan, and planning your Social Security benefits carefully, you can create a retirement plan that meets your needs and provides peace of mind for the future.

As you approach retirement, consider consulting with a top-rated FERS advisor who can provide personalized guidance and help you navigate the complexities of federal retirement planning. Whether you’re just starting your career or nearing retirement, making informed decisions now can secure your financial future and ensure a comfortable and fulfilling retirement.

To further enhance your understanding and make the most of your retirement planning, consider downloading our detailed eBook on FERS retirement strategies. This resource provides valuable insights tailored to federal employees and can help you make informed decisions that maximize your benefits.

Retirement is a journey, and with the right planning and resources, you can ensure that your journey is successful and rewarding. Let us help you navigate the path to a secure and prosperous retirement.

Advertisement

Search for Public Sector Retirement Expert.

Receive the Best advice.

PSR Experts can help you determine if Public Sector Retirement is right for you or if you should look for alternatives.

The Best Advice creates

the best results.

Search for Public Sector Retirement Expert.

Receive the Best advice.

PSR Experts can help you determine if Public Sector Retirement is right for you or if you should look for alternatives.

The Best Advice creates

the best results.

Advertisement

Recent Articles

3 Key Differences Between PSHB and FEHB That Every Postal Employee Should Be Aware Of

Key Takeaways

The transition from FEHB to PSHB

3 Major Retirement Planning Errors That Federal Employees Often Make—And How to Avoid Them

Key Takeaways:

Overlooking federal retirement calculations can lead

3 Things Every Federal Employee Needs to Know About Divorce and How It Affects Their Retirement Plans

Key Takeaways

Divorce can significantly impact your federal

What Federal Workers Are Doing to Keep Their FEHB Coverage Affordable as Costs Continue to Climb

Key Takeaways Federal employees and retirees can take strategic