Key Takeaways

- Your High-3 salary is the average of your highest-paid consecutive 36 months and is a key factor in determining federal retirement benefits.

- Understanding what counts toward your High-3 and knowing the rules for CSRS, FERS, and military credit can help you make more informed retirement decisions.

Many federal employees are surprised to learn that a single salary formula shapes their retirement: the high-3 calculation

- Also Read: Best Practices: Evaluating FEDVIP Coverage Pros, Cons, and Retiree Eligibility

- Also Read: Q&A: COBRA vs Immediate FEHB Continuation—What Federal Retirees Should Know

- Also Read: Annuity Options for Federal Retirees: How They Work and Risks to Consider

What Is the High-3 Salary Rule?

Definition of High-3 Salary

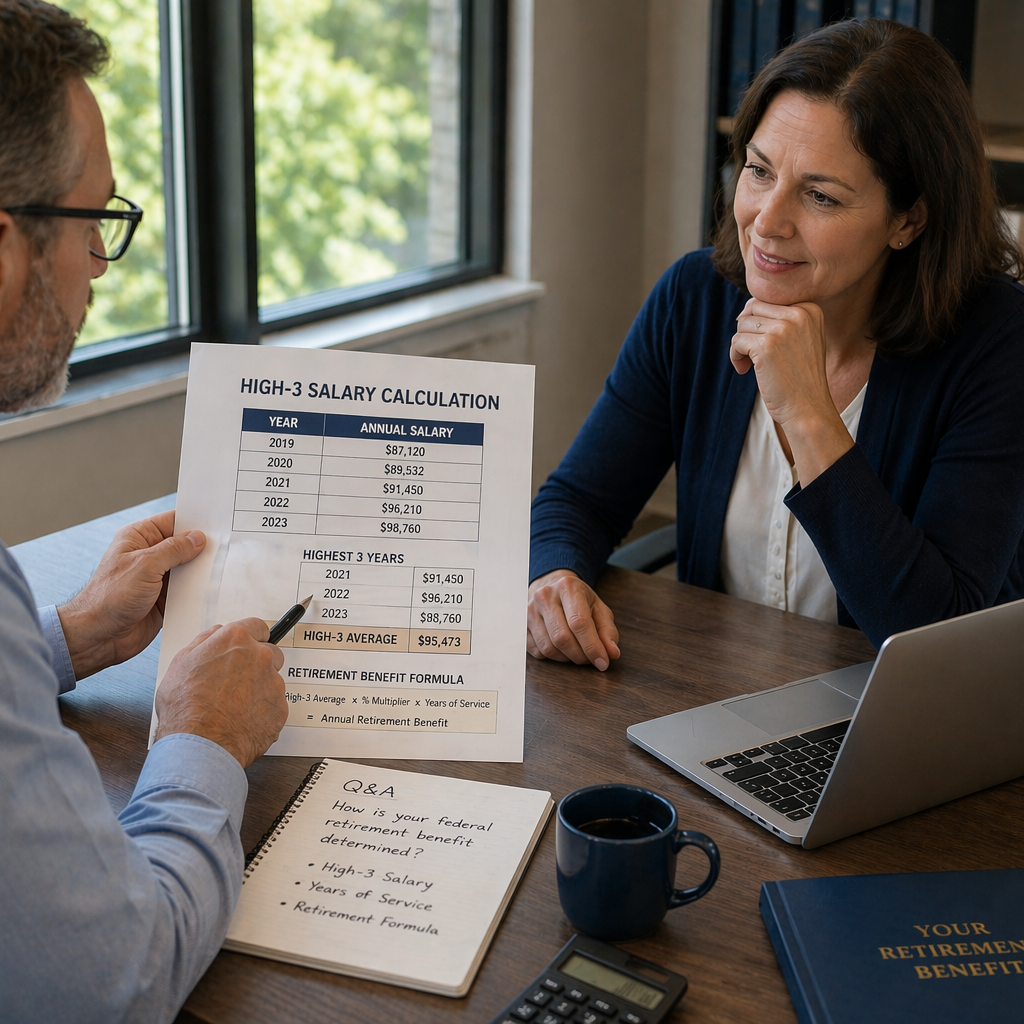

The “high-3 salary” rule refers to the average basic pay you earn during your highest-paid 36 consecutive months of federal service. This average does not include overtime, bonuses, or other forms of additional pay. Rather, it’s calculated using your base salary, locality pay, shift differentials if applicable, and any other consistent pay sources your position provides.

Who Uses the High-3 Calculation

The high-3 calculation is used for most federal retirement systems, including both the Civil Service Retirement System (CSRS) and Federal Employees Retirement System (FERS). Whether you work in a federal agency, the postal service, or another branch of government, your annuity will likely be based on this high-3 average.

How Is the High-3 Salary Computed?

Understanding Eligible Earnings

Eligible earnings for your high-3 calculation include only your “basic pay.” Basic pay typically covers your base salary and certain consistent allowances, like locality pay. It specifically excludes overtime, cash awards, bonuses, and certain types of premium pay. Understanding this distinction is crucial, as even periods with added performance bonuses will not boost your high-3 average.

Periods That Count Toward High-3

Only your highest-paid, consecutive 36 months count—these do not have to be your final three years, although they often are for many employees. If you received a significant pay increase earlier in your career, that stretch could form the backbone of your high-3, as long as the months are consecutive.

Why Does the High-3 Formula Matter?

Impact on Federal Retirement Benefit

Your high-3 average has a direct impact on your federal pension. The higher your high-3, the larger your retirement check will be, as it is a core input in your annuity calculation. Even small changes in basic pay can have a meaningful effect on your future income.

Factors Affecting Your Future Income

Several factors may influence your final high-3 figure, such as promotions, position changes, or taking on roles in higher locality pay areas. These changes can increase your average, ultimately affecting the base from which your pension is calculated.

What Factors Can Change High-3 Calculations?

Layoffs, Promotions, and Pay Changes

When you receive a promotion or move into a higher-paying position, that increased basic pay affects your high-3—provided the higher salary is consecutive and lasts at least 36 months. On the other hand, if you leave federal service (such as layoff or resign), your high-3 will reflect only the consecutive months you actually worked and received basic pay. Sudden pay reductions or changes in pay scale during that period will also impact your final calculation.

Leave Without Pay and Special Circumstances

Periods when you’re on Leave Without Pay (LWOP), or certain types of unpaid absences, typically are not included in high-3 calculations unless specifically credited by agency guidelines. Some special categories, like military duty or workers’ compensation, have distinct rules. It’s always important to check how an unusual leave situation may affect your high-3 accumulation period.

Are There Differences for CSRS and FERS?

Basic Comparison of Both Systems

Both CSRS and FERS use the high-3 concept, but the benefit formulas differ. CSRS, the older of the two, generally provides a higher benefit percentage based on years of service, while FERS offers a more integrated package with Social Security and a Thrift Savings Plan component. However, in both systems, the starting point for the annuity calculation is your high-3 average salary.

Implications for Benefit Calculations

If you’re under CSRS, your final pension is determined by multiplying your high-3 by a formula based on years and percentage rates. Under FERS, the same high-3 is used, but the benefit formula’s percentage factors are different. No matter your coverage system, knowing your high-3 is essential for projecting your retirement income.

What If You Have Military Service?

Military Service Credit in High-3

Federal employees with prior military service may be able to include that time toward their retirement eligibility and annuity calculation. However, for military time to count toward your high-3, you generally must make a deposit (buy back your service time) under federal guidelines. Once credited, this could impact your total years and, as a result, the size of your retirement benefit.

Steps to Include Military Time

To include your military service in your high-3 calculations, you need to request a military service credit deposit from your agency’s human resources department. It’s important to keep all service records and coordinate with your agency early to ensure the process is complete well before you retire.

How Can You Project Your Benefit?

Using Official Retirement Estimators

You can estimate your future benefit using official government calculators and retirement planning tools available through your agency or the Office of Personnel Management (OPM). These estimators let you input different salary and service combinations to better understand how choices today might affect your eventual retirement benefit.

Reviewing Your Earnings Record

Periodically review your earnings record and ensure all your federal service—and any applicable military service—is accurately documented. This habit not only gives you peace of mind before retirement but also helps catch and correct any errors well in advance.

Frequently Asked High-3 Questions

Common Myths and Clarifications

Many people believe that extra money like awards or overtime increases their high-3; however, only basic pay is counted. Another myth is that only the last three years count; in reality, it’s any consecutive 36 months, regardless of where they fall in your career.

Where to Find More Guidance

If you need further help understanding your high-3 or planning your retirement, each agency’s human resources office and the Office of Personnel Management provide educational materials and workshops. Rely on these official sources for the most up-to-date and accurate information.