1. You’re Responsible for Medicare Costs

Some Medicare services are free. No matter how much you contribute, you must pay a monthly premium. A percentage of your monthly wages is withheld to finance Social Security payments.

Annually, Medicare costs

- Also Read: Special Category Employees & Military: Comparing FERS and Military Retirement

- Also Read: Survivor Annuity Options and Costs: Guide for Federal Retirees in 2026

- Also Read: Comparing HSA Rules and FSA Rules: Key Differences for Federal Retirees

2. Unfortunately, Medicare Doesn’t Pay for Everything

Medicare Part A includes hospitals, home healthcare, nursing homes, and hospice care. The keyword here is “helps.” Medicare doesn’t cover everything. It covers most outpatient treatments (about 80 percent). You pay deductibles, co-pays, and co-insurance. If you’re sick, all these fees could add up.

Medicare Part B funds outpatient care, durable medical equipment, and preventive treatments like physicals. Again, “helps” is the key term. Medicare includes co-payments and coinsurance (up to 20 percent). Medicare does not cover eye and dental treatments.

3. Extra Cost for Coverage of Prescription Drugs

Part D, Medicare drug coverage, is separate insurance that must be purchased if you require coverage for prescription medications. When you enroll in Medicare for the first time, you will also be able to select the Part D prescription drug plan.

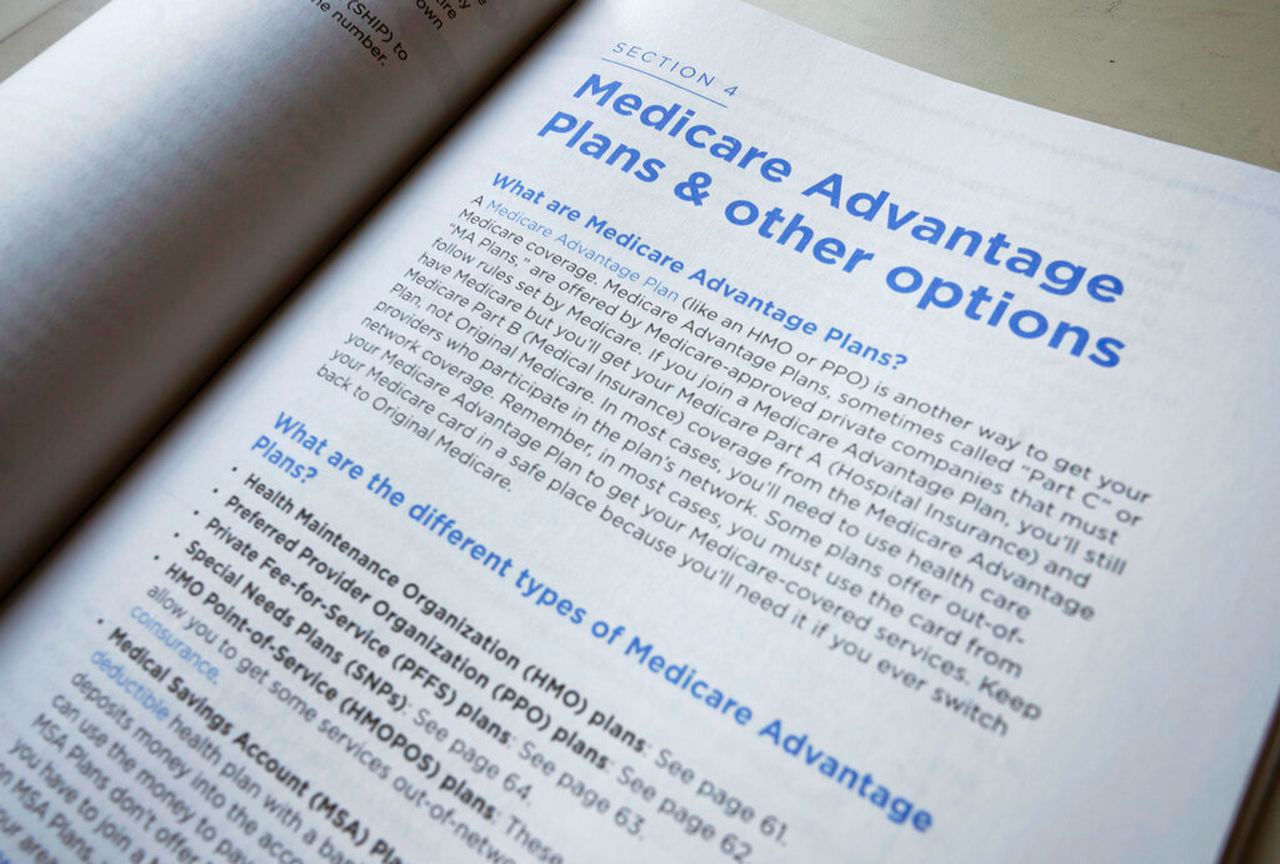

4. A Choice for Healthier Consumers

At 65, you can choose between regular Medicare and Medicare Advantage. Medicare Advantage differs from supplement plans (Medigap).

Medicare Supplement plans include co-payments and deductibles. Unlike original Medicare, your choice of doctors, healthcare providers, and treatment facilities will be limited. Medicare Advantage plans deal with different doctors and hospitals.

Medicare Advantage plans have modest monthly premiums and look comprehensive, yet they typically have high out-of-pocket expenses. Laboratory tests, x-rays, outpatient surgery, the ER, and other procedures have co-payments. Costs could mount.

5. Medicare coverage gaps are remedied by supplemental insurance

Private businesses offer Medigap policies and are meant to fill in the gaps left by Original Medicare. Medigap policies can assist with out-of-pocket expenses such as co-insurance and deductibles.

In contrast to Medicare Advantage plans, Medigap policies do not require members to join a particular medical network. They allow you to see any doctor or hospital participating in the original Medicare program. And a reference from your family doctor is not required.

Medigap policies are helpful for folks who are sick or have special medical requirements. They are adaptable and limit the amount of money the customer must pay out of pocket.

6. There are Constraints on Medigap Coverage

Medigap policies and Medicare Advantage plans are incompatible, unfortunately. There is no way to do both things.

Prescription medication coverage is not permitted in any newer Medigap policies. You must enroll in Medicare Part D or obtain separate prescription drug coverage if you need financial assistance to pay for your medications.

Vision and dental care are typically not covered by Medigap policies.

Emergency medical care incurred while abroad is covered by some Medigap policies. However, restrictions do apply. After a $250 deductible and up to $50,000 lifetime maximum, Medigap policies cover 80% of some emergency expenditures.

7. There are Penalties

It’s essential to enroll in Medicare Parts A, B, and D as soon as you become eligible for them.

The first part of the answer is that your premium may go up by 10%. If you don’t sign up for coverage for a full year, you could have to pay the higher cost for two years.

For Part B, you will be charged an extra 10% for every year that you were eligible for Part B but did not purchase it. It’s a permanent increase to your premium that you’ll have to pay for the rest of your life.

You may have to pay a penalty if you don’t have Part D or other drug coverage for more than 63 days after your original enrolment period. This fee is calculated by multiplying the “national base beneficiary premium” by the total number of months you were without Medicare Part D coverage. If you are enrolled in Medicare Part D, you will be responsible for the associated penalty.

You are automatically enrolled in Medicare if you are 65 or older. Medicare is a health insurance program for the elderly and handicapped. Most Medicare participants contribute through payroll taxes.

Contact Information:

Email: [email protected]

Phone: 9568933225

Bio:

Rick Viader is a Federal Retirement Consultant that uses proven strategies to help federal employees achieve their financial goals and make sure they receive all the benefits they worked so hard to achieve.

In helping federal employees, Rick has seen the need to offer retirement plan coaching where Human Resources departments either could not or were not able to assist. For almost 14 years, Rick has specialized in using federal government benefits and retirement systems to maximize retirement incomes.

His goals are to guide federal employees to achieve their financial goals while maximizing their retirement incomes.