Key Takeaways

- Understanding your high-3 salary is crucial for federal pension accuracy and effective retirement planning.

- Weighing the pros and cons of high-3 helps you make informed decisions about your future benefits.

The “high-3” salary rule plays a central role in how your federal pension is calculated. If you’re a federal employee or retiree, knowing how this rule works can make a significant difference in your retirement planning. Let’s break down what the high-3 rule is, why it matters, and how it might affect your retirement income.

What Is the High-3 Salary Rule?

Definition of High-3 Salary

- Also Read: Special Category Employees & Military: Comparing FERS and Military Retirement

- Also Read: Survivor Annuity Options and Costs: Guide for Federal Retirees in 2026

- Also Read: Comparing HSA Rules and FSA Rules: Key Differences for Federal Retirees

Your “high-3 salary” refers to the highest average basic pay you’ve earned during any three consecutive years of federal service. These three years don’t have to be your final years before retirement, but they often are, because pay rates tend to rise throughout your career.

Who Determines High-3 Calculation

The Office of Personnel Management (OPM) is responsible for defining and applying the high-3 calculation as it pertains to federal retirement benefits. Your agency keeps records of your earnings and forwards this information to OPM to help ensure your pension amount is computed correctly.

Which Earnings Are Included

Only your basic pay counts toward the high-3. This includes your base salary and certain types of regular pay, such as locality pay, but excludes overtime, bonuses, and allowances. If you have questions about what is counted, it’s always a good idea to check with your human resources department.

How Does High-3 Affect Pensions?

Role in Pension Calculation

Under both the Federal Employees Retirement System (FERS) and the Civil Service Retirement System (CSRS), your high-3 serves as the foundation for estimating your monthly pension. Agencies use your average high-3 salary, along with your years of credited service and a set formula, to calculate your retirement payment.

Importance for Retirement Planning

Knowing your likely high-3 average helps you estimate your future pension. This understanding can help you set realistic expectations and make strategic decisions about your retirement timing or potential career moves. For example, an increase in your salary near the end of your career could impact your high-3 and your future pension.

Possible Impact on Future Benefits

If your most recent three years of service are your highest paid, your pension calculation will reflect your peak earnings. However, if you experience a salary drop or leave government service before your earning peak, your pension could be lower than you expect. This makes it important to plan carefully around your high-3 period.

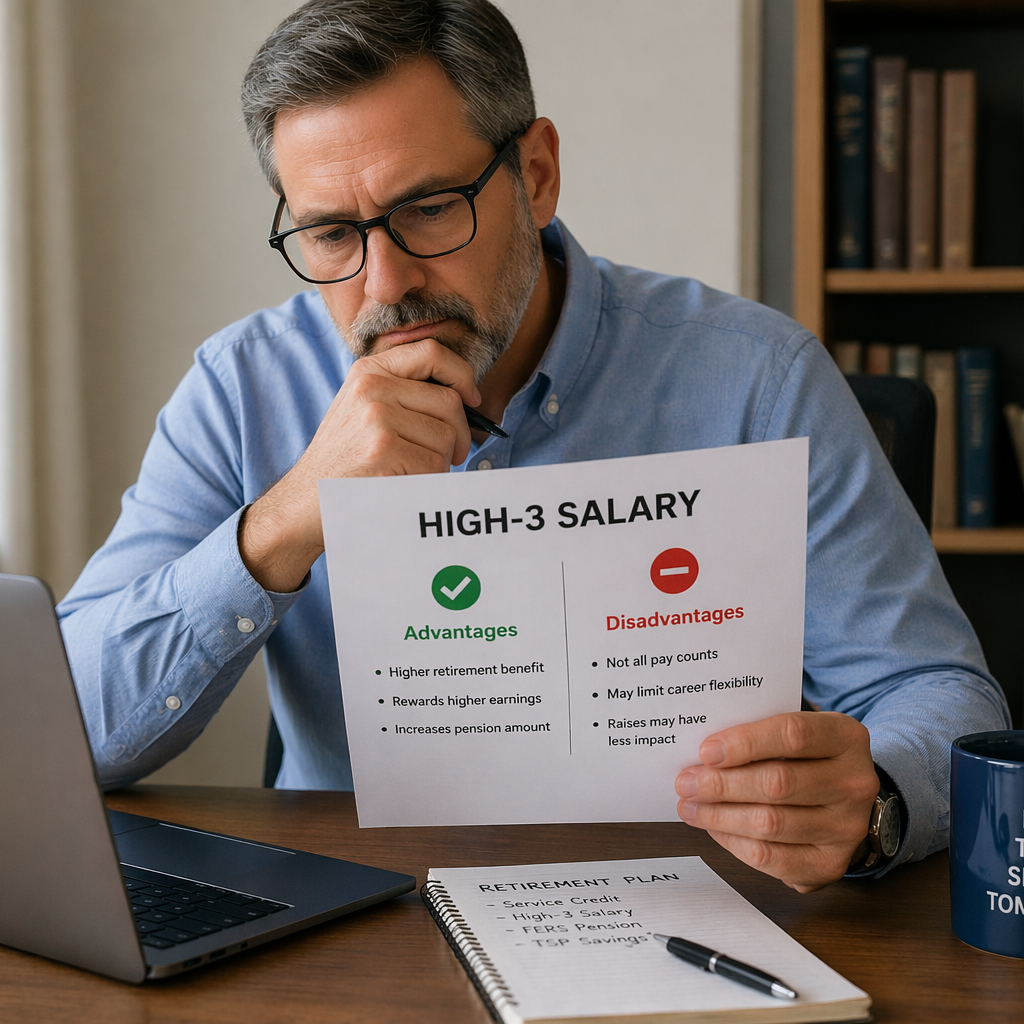

What Are the Pros of High-3 Salary?

Predictable Income Calculation

The high-3 rule offers a straightforward and predictable method for determining pension benefits. Both you and your agency know exactly how your average pay is used, which increases transparency and reduces uncertainties about how retirement income is figured.

Potential for Higher Pension Amounts

If you earn your highest pay toward the end of your career — which is common in government jobs — the high-3 rule likely leads to an increased pension. Planning promotions, job changes, or locality moves during your top earning phases can work in your favor.

Transparency in Benefit Formulas

With the high-3 approach, there’s minimal guesswork. The calculation process is outlined in federal retirement guides, and the rules are consistent across employee types and agencies. This transparency empowers you to follow your own numbers over time.

What Are the Cons of High-3 Salary?

Limited Inclusion of Overtime

Overtime, bonuses, and some incentive payments are usually not counted toward your high-3 salary. If your compensation comes largely from these sources, your high-3 computation may not reflect your actual recent income, resulting in a smaller pension than anticipated.

Possible Lower Payouts for Late Career Earners

If you experienced a significant pay increase late in your career but didn’t maintain that pay for three consecutive years, those higher earnings may not help much in your high-3 calculation. Career interruptions or significant pay changes just before retirement can limit how much your pension grows.

Challenges for Variable Income Roles

Some federal positions (like certain law enforcement or shift-based jobs) experience frequent changes in basic pay due to assignment premiums or differential pay. If your pay level has fluctuated over your career, the high-3 average may not match what you consider to be your typical annual income.

Is High-3 Salary Right for You?

Reviewing Your Career Timeline

Timing is everything. Review your career to pinpoint your highest three-year earning period. If you’re approaching retirement, it may make sense to time your departure after three consecutive years of top earnings, if you can.

Assessing Pension Scenarios

Run retirement projections using your potential high-3 average to see how different scenarios could impact your future benefits. Consider if staying longer or seeking new assignments could meaningfully increase your high-3 and, in turn, your pension.

Questions to Discuss with Advisors

Bring your pay history, career goals, and intended retirement timeline to your benefits advisor or financial professional. Ask specific questions like: “When was or will be my high-3 period?” and “How can changes in my role affect my high-3 calculation?” Getting clarity now avoids surprises later.

High-3 vs. Other Federal Benefit Calculations

High-3 Compared to High-5

Some retirement systems or prior federal programs use a “high-5” calculation — the five highest consecutive years of average salary — instead of the three that current systems use. The high-3 method often produces a higher average and, therefore, potentially higher pension payments, but it also can be more sensitive to short-term pay fluctuations.

Impact on Thrift Savings Plan (TSP)

While your high-3 determines your pension, your TSP account is separate. Contributions to your TSP are based on your actual earnings, not just your high-3. It’s important to plan for both your pension and TSP savings as part of a comprehensive retirement strategy.

Other Federal Retirement Metrics

Beyond the high-3, federal retirement calculations may reference total service years, age at retirement, and eligibility criteria. For some special positions, such as law enforcement or air traffic controllers, other pay metrics or formulas may apply. Reviewing all your benefit statements gives a complete picture.