Key Takeaways:

-

Early retirement is achievable for federal employees with smart financial planning and leveraging existing benefits.

-

Creative strategies such as maximizing the Thrift Savings Plan (TSP) and understanding retirement eligibility options can significantly impact your retirement timeline.

Understanding the Basics of Federal Retirement

- Also Read: How-to Compare Inflation Protection Strategies for Federal Retirees in 2026

- Also Read: Health Expense Budgeting: 8 Tips for Retirees Planning Medical Costs

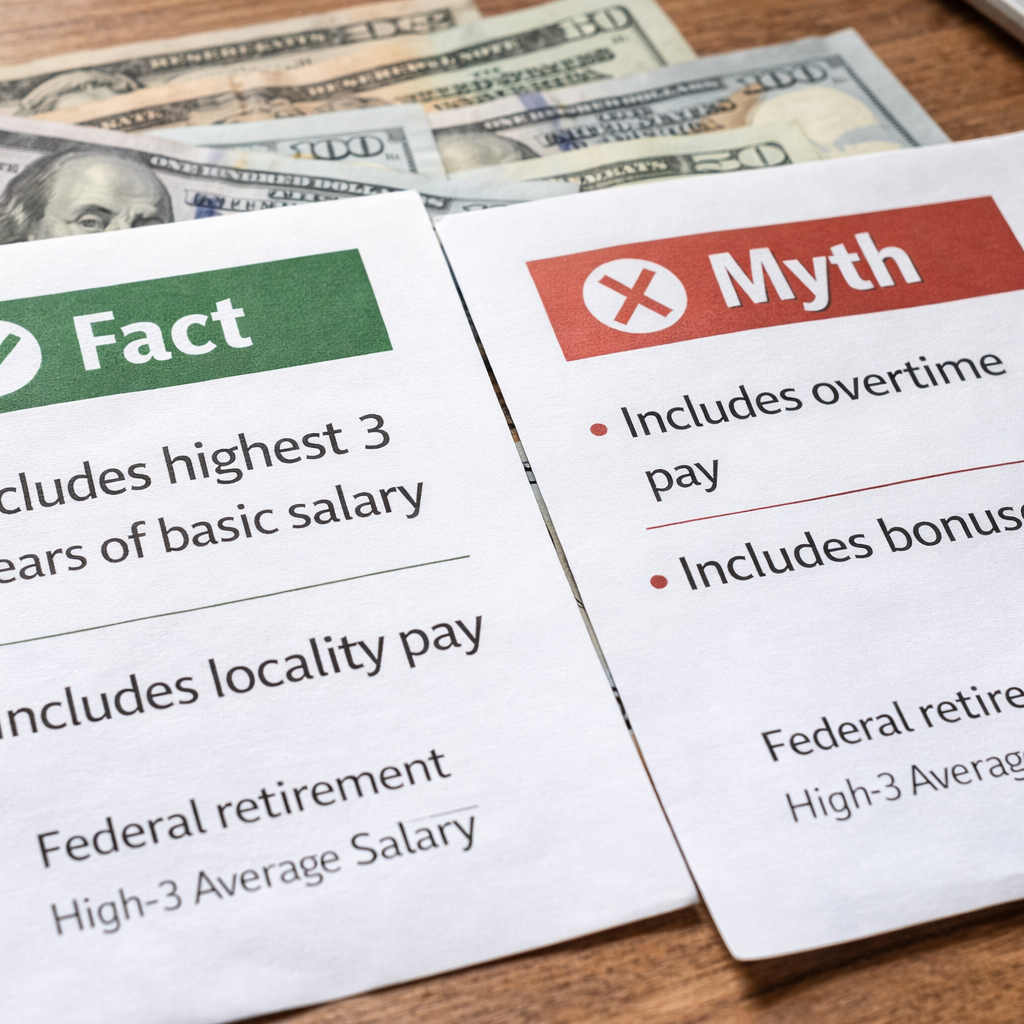

- Also Read: High-3 Average Salary Explained: Myths vs Facts for Federal Retirement

Under FERS, your retirement package typically includes three key components:

-

FERS Basic Annuity: Calculated based on your years of service and the high-three average of your salary.

-

Social Security: Benefits you become eligible for after age 62.

-

TSP Contributions: Your personal savings, boosted by government contributions.

CSRS, though now phased out, offers a more substantial annuity for those still enrolled but does not include Social Security.

Early Retirement Options for Federal Employees

The concept of early retirement in federal service comes with several paths, each with its own eligibility requirements and financial implications. These include:

Minimum Retirement Age (MRA) +10

This option allows FERS employees to retire as early as age 57 (depending on your birth year) with at least 10 years of service. While you can claim an annuity, it comes with a reduction of 5% for every year you’re under age 62.

Voluntary Early Retirement Authority (VERA)

VERA is a program designed to encourage early retirement during workforce restructuring. It’s available to employees as young as 50 with at least 20 years of service or at any age with 25 years of service.

Special Provisions for Certain Employees

Law enforcement officers, firefighters, and air traffic controllers can retire early due to the demanding nature of their jobs. These employees can retire after 20 years of service at age 50 or after 25 years of service at any age.

Boosting Your Thrift Savings Plan (TSP)

The TSP is a cornerstone of federal retirement planning and can be your ticket to early retirement. By maximizing your TSP contributions, you’ll build a substantial nest egg to support your retirement goals.

Increase Your Contributions

For 2025, the TSP contribution limit is $23,500, with an additional $7,500 catch-up contribution for those aged 50 and older. If you’re aged 60-63, the SECURE 2.0 Act allows for even higher catch-up contributions. Maximize these limits to accelerate your savings.

Consider the Roth Option

The Roth TSP allows you to contribute post-tax dollars, ensuring tax-free withdrawals during retirement. This is especially beneficial if you anticipate being in a higher tax bracket later.

Take Advantage of Matching Contributions

The government matches up to 5% of your contributions under FERS. This is essentially free money that can significantly grow your savings over time.

Strategic Use of Leave and Benefits

Your accumulated leave and other benefits can play a vital role in your early retirement strategy. Here’s how:

Lump-Sum Payouts for Annual Leave

Upon retirement, you’re entitled to a lump-sum payment for your unused annual leave. This can provide a financial cushion as you transition into retirement.

Sick Leave Credit

Unused sick leave is added to your total years of service, increasing your annuity. This benefit is especially valuable for those nearing eligibility thresholds.

Health Insurance (FEHB) and Medicare Coordination

Continuing your Federal Employees Health Benefits (FEHB) coverage into retirement ensures comprehensive healthcare. Once eligible for Medicare, coordinating it with FEHB can reduce out-of-pocket costs.

Reducing Living Expenses

Early retirement requires a clear understanding of your post-retirement budget. Here are ways to cut costs:

-

Downsizing: Consider moving to a smaller home or relocating to an area with a lower cost of living.

-

Eliminating Debt: Pay off high-interest debt before retirement to free up more income.

-

Lifestyle Adjustments: Small changes, such as limiting discretionary spending, can add up over time.

Exploring Alternative Income Streams

Retiring early doesn’t mean you have to stop earning. Supplementing your annuity and TSP withdrawals with alternative income can make early retirement more feasible.

Part-Time Work

Many retirees take on part-time jobs or consulting roles to stay active and generate income.

Rental Income

Investing in real estate can provide a steady income stream.

Passive Income

Consider dividends from investments, royalties, or online businesses as potential income sources.

Planning for Social Security Benefits

While Social Security isn’t available until age 62, planning for it is essential, especially if you’re retiring early. Delaying benefits can increase your monthly payments, while taking them early reduces the amount. Ensure your retirement strategy aligns with your Social Security goals.

Calculating Your Retirement Budget

A detailed budget is critical for determining the feasibility of early retirement. Estimate your monthly expenses, including:

-

Housing costs

-

Healthcare and insurance premiums

-

Food and utilities

-

Discretionary spending

Compare this with your expected income from your annuity, TSP, and other sources. Use conservative estimates to account for inflation and unexpected costs.

The Importance of Financial Advisors

Retirement planning can be complex. Consulting with a financial advisor experienced in federal benefits can help you:

-

Understand your retirement eligibility and options.

-

Maximize your benefits and savings.

-

Create a sustainable withdrawal strategy.

Staying Flexible in Your Plans

Retirement is a journey, not a fixed destination. Stay open to revising your plans as circumstances change. Whether it’s market fluctuations, policy updates, or personal needs, adaptability is key to a successful early retirement.

Retiring Early Without Compromising Financial Security

Early retirement is a dream for many federal employees, but it’s one that requires careful planning and strategic decision-making. By leveraging your federal benefits, maximizing your savings, and exploring creative strategies, you can achieve financial independence and enjoy your retirement years on your terms.