Key Takeaways

- Understanding the High-3 Average Salary is crucial for accurate federal retirement planning.

- Not all pay types or years count toward your High-3; careful record review is essential.

Many federal employees misunderstand which years and pay types count toward their High-3 average salary. By clearing up the myths and revealing the facts, you can approach your retirement decisions with greater confidence and clarity. Let’s break down exactly how the High-3 works.

What Is the High-3 Average Salary?

Definition and calculation basics

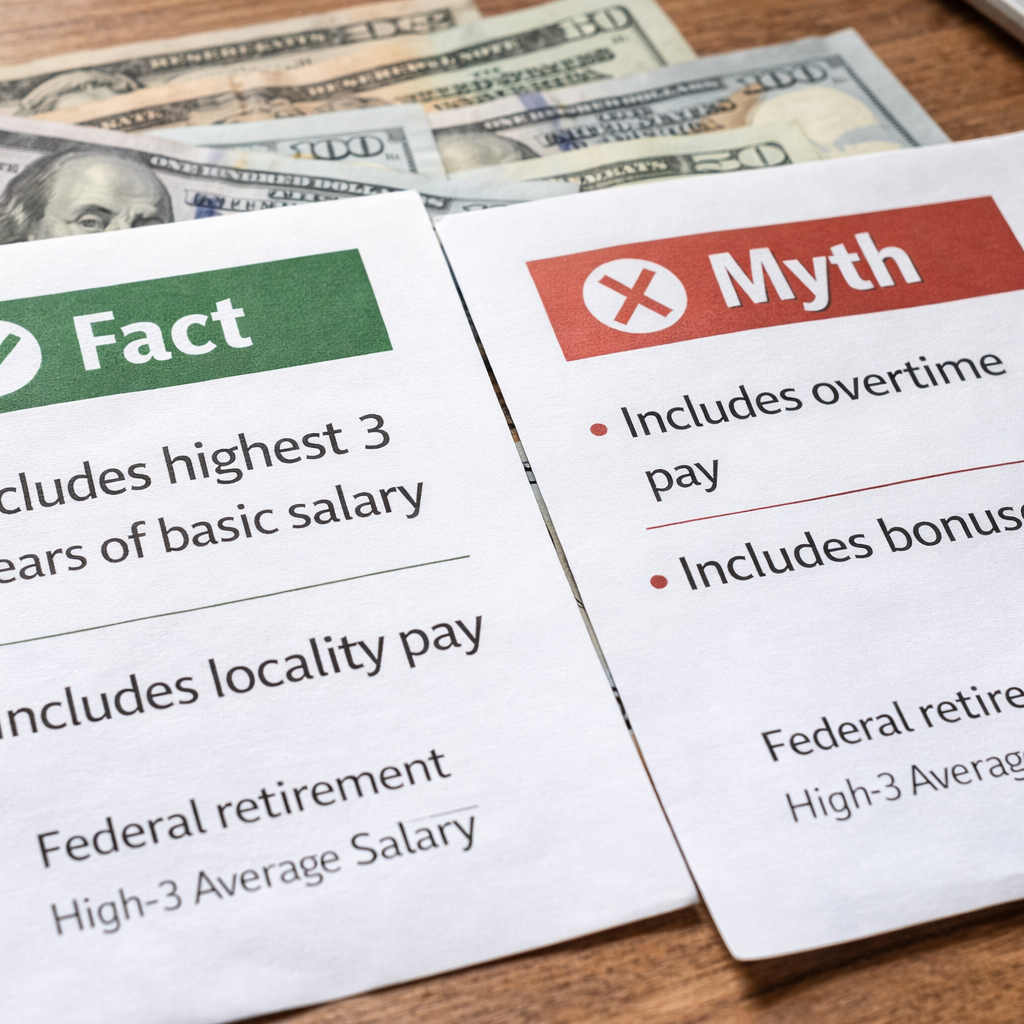

The High-3 Average Salary is the average of your highest-paid consecutive 36 months of basic pay during your federal career. “Basic pay” refers to your regular rate of pay, including certain locality adjustments and shift differentials, but not bonuses or overtime. This calculation sets the foundation for several federal retirement benefits.

- Also Read: Q&A: COBRA vs Immediate FEHB Continuation—What Federal Retirees Should Know

- Also Read: Annuity Options for Federal Retirees: How They Work and Risks to Consider

- Also Read: Case Study: Prescription Drug Coverage Coordination Tips for Federal Retirees

Who uses the High-3 formula

Federal retirement systems such as the Civil Service Retirement System (CSRS) and the Federal Employees Retirement System (FERS) both rely on the High-3 formula. Most full-time, part-time, and some temporary federal employees—across government agencies—have their retirement packages calculated using this approach. Understanding your High-3 ensures you won’t be caught off guard by miscalculations when you’re ready to retire.

Why Does the High-3 Matter for Retirement?

Impact on your federal annuity

Your High-3 plays a direct and critical role in how your federal annuity is calculated. In most cases, this figure is multiplied by a formula based on your years of credible service and a percentage set by your retirement system. If your High-3 is higher, your base retirement income will likely be higher, too. This is why monitoring your pay records and understanding what affects your High-3 can make a meaningful difference in your future benefits.

Connection to other retirement benefits

The High-3 doesn’t just affect your main retirement annuity. Other benefits, such as survivor annuities and, in some cases, disability benefits, may also be tied to this average. Knowing precisely what’s included enables you and your loved ones to plan appropriately, especially when considering which periods or types of service contribute most to your retirement picture.

What Are Common Myths About High-3?

Myth: Bonuses always count toward High-3

A frequent misconception is that performance awards, recruitment bonuses, or retention incentives are always part of your High-3. In reality, these forms of compensation—while rewarding—are not considered basic pay and generally do not count toward your High-3 calculation. Only your regulated base salary and its qualified increases are factored in.

Myth: High-3 includes all types of pay

While some believe that every dollar earned—like overtime, hazard pay, or allowances—is counted, that’s not correct. The government only uses basic pay, which excludes overtime, holiday pay, travel stipends, and most one-time payments. Understanding the exact definition of basic pay helps you avoid overestimating your retirement figures.

Myth: Only your last three years matter

Many employees assume their High-3 must be based on their final three years before retirement. While those years are often the highest earning for many, the calculation can actually use any 36-month consecutive period in your career. For some, earlier years with highest-grade or special assignment pay deliver a higher average than their final years.

What Are the Facts About High-3?

How service periods are selected

Your High-3 is based on whichever 36 consecutive months of service yield the highest average basic pay. These months do not have to align with calendar or fiscal years, and they may start or end at any point across your federal tenure. This offers some flexibility, especially if you changed roles or locations throughout your career.

Types of pay included in High-3

The only earnings included in your High-3 calculation are your basic pay. This may include locality pay adjustments, shift differentials, and—in some cases—certain kinds of special pay, depending on your position. It never includes overtime, bonuses, cash awards, travel reimbursements, or other irregular pay.

How breaks in service affect High-3

You can have breaks in your federal service and still have them factored into your overall retirement calculation. But for High-3 purposes, only periods of actual federal service count—so any gaps (such as resignations or extended unpaid leave) are ignored in the consecutive month count. Your 36-month period must be consecutive paid months of qualifying service.

How Can You Estimate High-3 Yourself?

Gathering your pay records

Start by collecting your earning statements, W-2s, or official service records for your federal career. Make sure you focus on the basic pay listed (and not extras like overtime or bonuses) for each year. It may help to create a spreadsheet with yearly and monthly breakdowns.

Calculating your average step by step

- Identify every 36-consecutive-month period and mark the basic pay received in each month.

- Add the total basic pay earned during those months.

- Divide the sum by 36 to find your High-3 average monthly salary.

If you used annual salary figures, multiply by 3 (for three years) and then divide by 36 (months), or divide your total by 3 for the annual High-3.

Common pitfalls in self-estimation

One of the main missteps is accidentally including non-basic pay items like overtime, bonuses, or special incentive payments. Another pitfall is not using consecutive months—gaps in service don’t count, so skipping months or using “best” individual months (rather than consecutive ones) leads to incorrect results. Double-check your math and confirm the official definition of “basic pay” for your position.

Can Part-Time or Interrupted Service Affect High-3?

Effect of part-time schedules

If you worked part-time for any stretch, your basic pay is prorated to reflect your work schedule. While the calculation formula stays the same, your High-3 will be based on what you actually earned during those months—not what you would have made working full-time. This can lower your High-3 average if a significant period of your highest pay years was part-time.

Periods of leave without pay

If you took extended leave without pay, those months generally aren’t counted toward your High-3 period, since you didn’t receive basic pay. Your High-3 window would skip these months and continue once your paid service resumes.

Impact of breaks in federal service

Any official break—such as resignation or temporary separation—interrupts your High-3. The 36 months must be consecutive, so breaks in service mean you need to find a new block of qualifying months. Service before and after a break counts toward your total service time, but only consecutive paid service counts for High-3 purposes.