Key Takeaways:

- Divorce can significantly impact your federal retirement benefits, including your pension, Thrift Savings Plan (TSP), and insurance policies.

- Understanding how your federal benefits are divided and protected in a divorce can help you safeguard your financial future.

Divorce Can Wreck Your Retirement—Here’s What Federal Workers Need to Know to Protect Their Benefits

Divorce is never easy, but for federal employees, it can come with an additional layer of complexity—one that can have lasting effects on your retirement. If you’re a federal worker going through or considering a divorce, it’s essential to understand how your benefits, pension, and retirement savings could be affected. Whether it’s the division of your Thrift Savings Plan (TSP), survivor benefits, or the impact on your Federal Employees Retirement System (FERS) pension, the financial consequences of divorce can be severe. Here’s what you need to know to ensure your retirement remains intact, even if your marriage doesn’t.

How Your Pension Could Be Divided

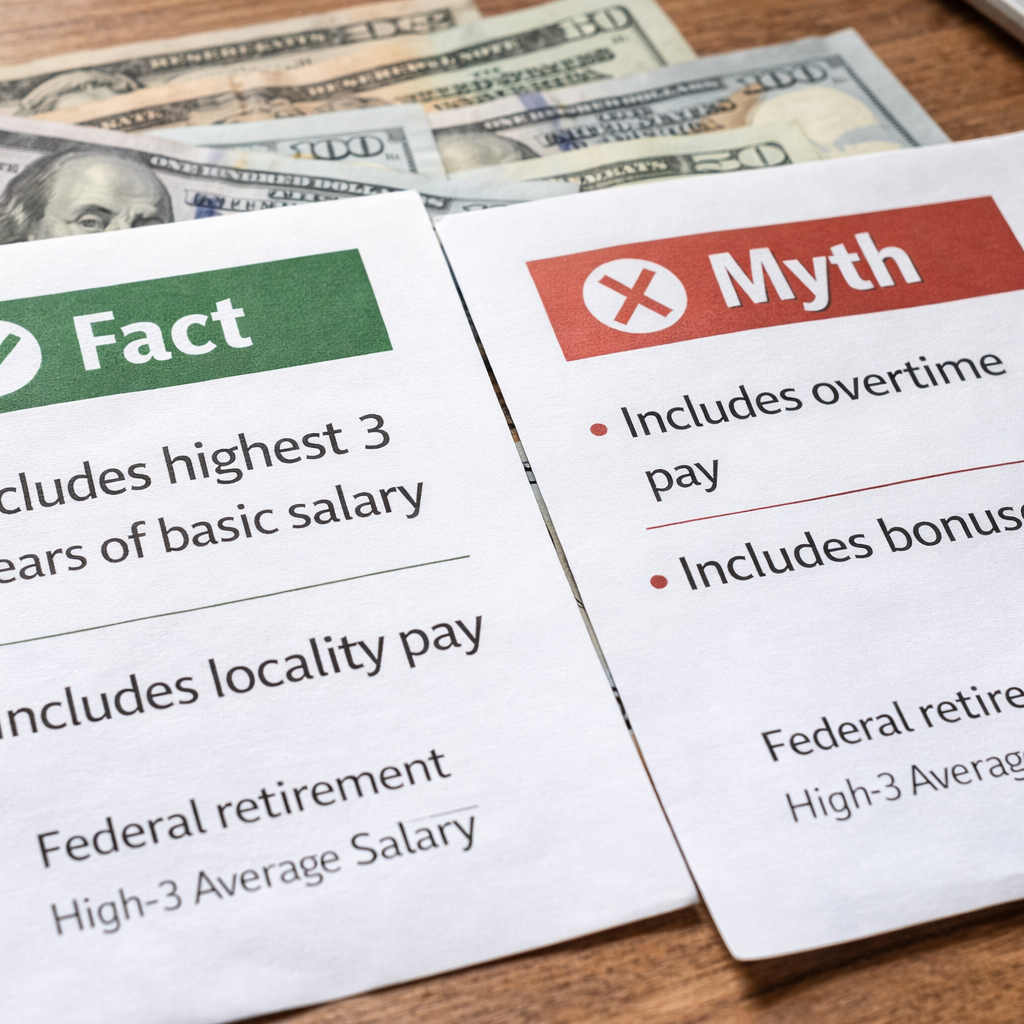

For federal employees, one of the biggest concerns during a divorce is how the FERS or CSRS pension will be divided. Under federal law, your pension can be considered a marital asset and may be subject to division in the divorce settlement. This division is typically spelled out in a court order, known as a Court Order Acceptable for Processing (COAP), which determines how much of your pension your ex-spouse will receive.

In most cases, the pension is divided based on the length of the marriage and the number of years you’ve worked as a federal employee during that time. For example, if you were married for 15 years and worked as a federal employee for 10 of those years, a portion of your pension could be allocated to your former spouse. However, the exact terms will depend on your divorce settlement and state laws.

To protect yourself, it’s crucial to work with an experienced attorney who understands federal benefits and can ensure your pension is handled fairly in the divorce. It’s also important to update your beneficiary information immediately after the divorce to prevent any unintended consequences.

The Thrift Savings Plan (TSP): A Target for Division

The Thrift Savings Plan (TSP) is another asset that’s often divided in a divorce. Just like a 401(k) in the private sector, the TSP is a defined contribution plan that accumulates over the years, with contributions from both you and your federal employer. And, just like other retirement savings, it can be considered a marital asset and split between you and your ex-spouse.

When a TSP is divided, it’s typically done through a court-ordered process that allocates a portion of your account balance to your former spouse. This process is known as a Retirement Benefits Court Order (RBCO), and it outlines exactly how much of your TSP should be transferred.

The good news is that the division of a TSP is done through a rollover, which means there are no immediate tax implications for either party. However, it’s still essential to understand the terms of the division, as losing a significant portion of your TSP balance could affect your long-term retirement goals.

Survivor Benefits: What You Need to Know

Survivor benefits are another area where divorce can dramatically impact your retirement planning. If you’re a federal employee, your spouse may have been entitled to survivor benefits, which ensure that they receive a portion of your pension after your death. However, after a divorce, you’ll need to reassess how these benefits are distributed.

Federal employees under FERS can elect to provide their ex-spouse with survivor benefits, but this decision must be made carefully. In some cases, a divorce settlement will require you to continue providing these benefits to your former spouse, which will reduce the amount of your monthly pension. On the other hand, if you want to eliminate these benefits entirely, you must specify this in your court order, or the benefits could automatically continue.

For those under the CSRS system, the rules are similar. You’ll need to decide whether to maintain survivor benefits for your ex-spouse, which could significantly impact the total amount of your pension. Be sure to review your options carefully and work with a legal professional to make the best decision for your financial future.

Impact on FEHB Coverage

Federal Employees Health Benefits (FEHB) coverage is another crucial element to consider during a divorce. While federal employees enjoy comprehensive health insurance through the FEHB program, your ex-spouse will lose access to this coverage once the divorce is finalized. This means that they’ll need to find new health insurance, either through their own employer or the private market.

It’s important to note that your children can still be covered under your FEHB plan, but your ex-spouse will not. Additionally, if your ex-spouse qualifies for temporary continuation of coverage (TCC), they can maintain FEHB for up to 36 months after the divorce, but they’ll be responsible for the full premium cost, which is typically much higher than the employee rate.

If you’re the one losing FEHB coverage due to divorce, be sure to explore your options early to avoid any gaps in coverage. This is especially important if you’re nearing retirement, as healthcare costs can quickly become one of the most significant expenses in your retirement years.

Protecting Your FEGLI Benefits

The Federal Employees’ Group Life Insurance (FEGLI) is another benefit that can be affected by divorce. If your ex-spouse was listed as a beneficiary on your life insurance policy, you’ll need to update your beneficiary information as soon as possible. Otherwise, your ex could remain the primary beneficiary, even after the divorce is finalized.

Federal employees have the ability to change their FEGLI beneficiary at any time, so don’t delay in making these updates. If you’re unsure how to go about this, your human resources department can guide you through the process. Additionally, if you’re required to maintain life insurance coverage for your ex-spouse as part of your divorce settlement, be sure to review your options and consider whether additional coverage is needed to meet your obligations.

Be Proactive About Your Retirement Plans

Divorce can have a lasting impact on your federal retirement benefits, but the key to protecting yourself is to be proactive. Start by reviewing your current benefits, including your pension, TSP, and insurance policies, and determine how they might be divided in a divorce. Then, work with a knowledgeable attorney to ensure that your interests are protected and that you understand the long-term financial implications.

Updating your beneficiary information, understanding the division of assets, and exploring your healthcare options are all critical steps in securing your retirement future after a divorce. By taking the right steps now, you can ensure that your federal benefits remain a source of stability, even in the face of life’s most challenging transitions.

Safeguarding Your Retirement After Divorce

While divorce can introduce financial uncertainty, federal employees have tools at their disposal to protect their retirement benefits. Whether it’s dividing your pension fairly, managing the impact on your TSP, or updating your life insurance beneficiaries, careful planning can help you safeguard your financial future. With the right strategy, you can navigate the complexities of divorce without derailing your retirement.