It makes sense to worry about running out of money in retirement. But you can restate your worries by creating a well-thought-out retirement income strategy.

Most people work for at least 35 to 45 years. They are entitled to enjoy an exceptional retirement when this long journey is finally over. The rewards of your decades of work may be fairly satisfying if you are careful with your saving and general retirement planning.

Here are five steps to planning an enjoyable retirement without the fear of running out of money.

1. Set your priorities

- Also Read: How-to Compare Inflation Protection Strategies for Federal Retirees in 2026

- Also Read: Health Expense Budgeting: 8 Tips for Retirees Planning Medical Costs

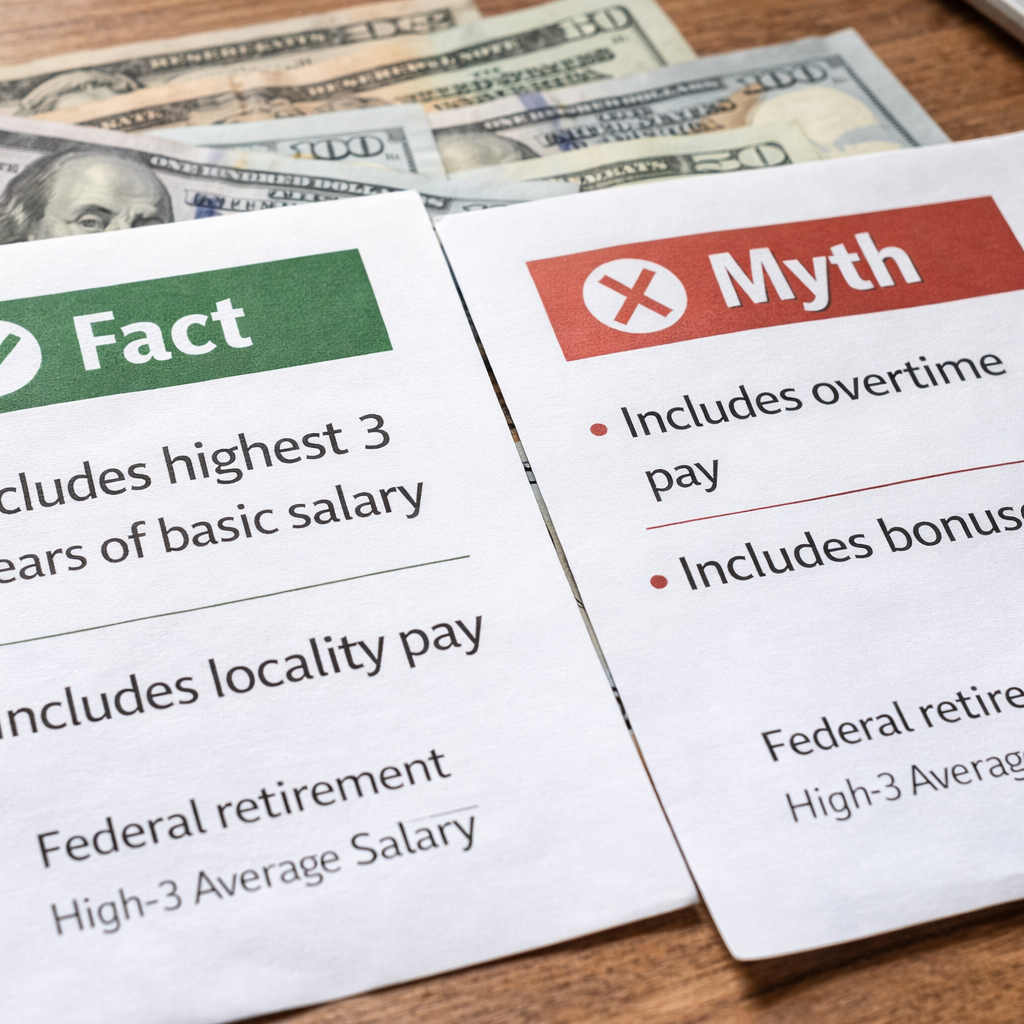

- Also Read: High-3 Average Salary Explained: Myths vs Facts for Federal Retirement

It also helps to have an open discussion with your partner to determine what is essential to you both. The top four issues that are essential to you should be listed and discussed as a group.

2. Manage your portfolio

One reliable source of income comes from a collection of principal-guaranteed CDs, fixed annuities, market-linked CDs, and fixed-index annuities. Growth accounts, where investments like equities that can change in value are kept, are in the other bucket.

The plan is to take distributions out of the cash pot but not the stock one. When the market rises, the stock bucket may be partially liquidated as needed to refill with cash.

Keeping the withdrawal rate under control during the distribution period is crucial to prevent running out of retirement funds throughout your lifetime.

3. Convert to Roth IRA

For three main reasons, it is sensible to convert some of your traditional IRA to a Roth IRA over several years before retirement.

1. Your Roth will grow entirely tax-free.

2. If you are 59½ years old or older and can wait at least five years following the conversion, any retirement income you withdraw from the account will be free of taxes and penalties.

3. Beneficiaries will receive the gift of funds from a Roth IRA tax-free.

Yes, you must pay taxes on the amount you convert to a Roth, but because they are historically low right now, you may be able to save money in retirement by paying the taxes now rather than later. Instead of doing everything at once, it is advisable to convert over several years. This allows you to reduce your tax payment and choose how much to convert each year based on your tax rate.

4. Be prepared for and protected from the worst

How would your money fare if a situation similar to the financial crisis of 2008 arose? Your plan will fail if all of your money is invested in equities. You can defend against a downturn by moving money out of your principal-guaranteed accounts.

At the same time, you shouldn’t sell shares to pay bills because doing so when the value of those shares is lower means you will have fewer shares to profit from when the stock market recovers. Bonds are currently not safe, despite what the general public believes, as interest rates are rising. Bond prices often drop as interest rates rise.

Planning for circumstances with volatility can be made easier by developing a solid distribution strategy. You can be more conservative or set aside a few years’ worth of cash payouts if you know how your account balances might be impacted in years when your investments experience a loss.