Key Takeaways

-

Locality pay may soon be excluded from pension calculations under new legislative proposals, threatening retirement income for employees in high-cost living areas.

-

Government employees nearing retirement should monitor these developments closely, as they may need to adjust financial plans or retirement dates to mitigate potential losses.

Locality Pay Was Designed to Balance Cost-of-Living Gaps

For decades, locality pay has been a critical component of total compensation for public sector employees working in areas with high living costs. Introduced to reduce federal pay disparities across geographic regions, it ensures that employees in places like New York City or San Francisco are not unduly penalized for local economic conditions.

- Also Read: Installment Payments vs TSP Annuity: Myths and Facts for Federal Retirees

- Also Read: How-to Compare Inflation Protection Strategies for Federal Retirees in 2026

- Also Read: Health Expense Budgeting: 8 Tips for Retirees Planning Medical Costs

Although considered part of regular earnings during employment, locality pay is not guaranteed to be included in the computation of your retirement annuity. That inclusion currently depends on your individual pay structure and the proposed legislative changes that are now gaining traction.

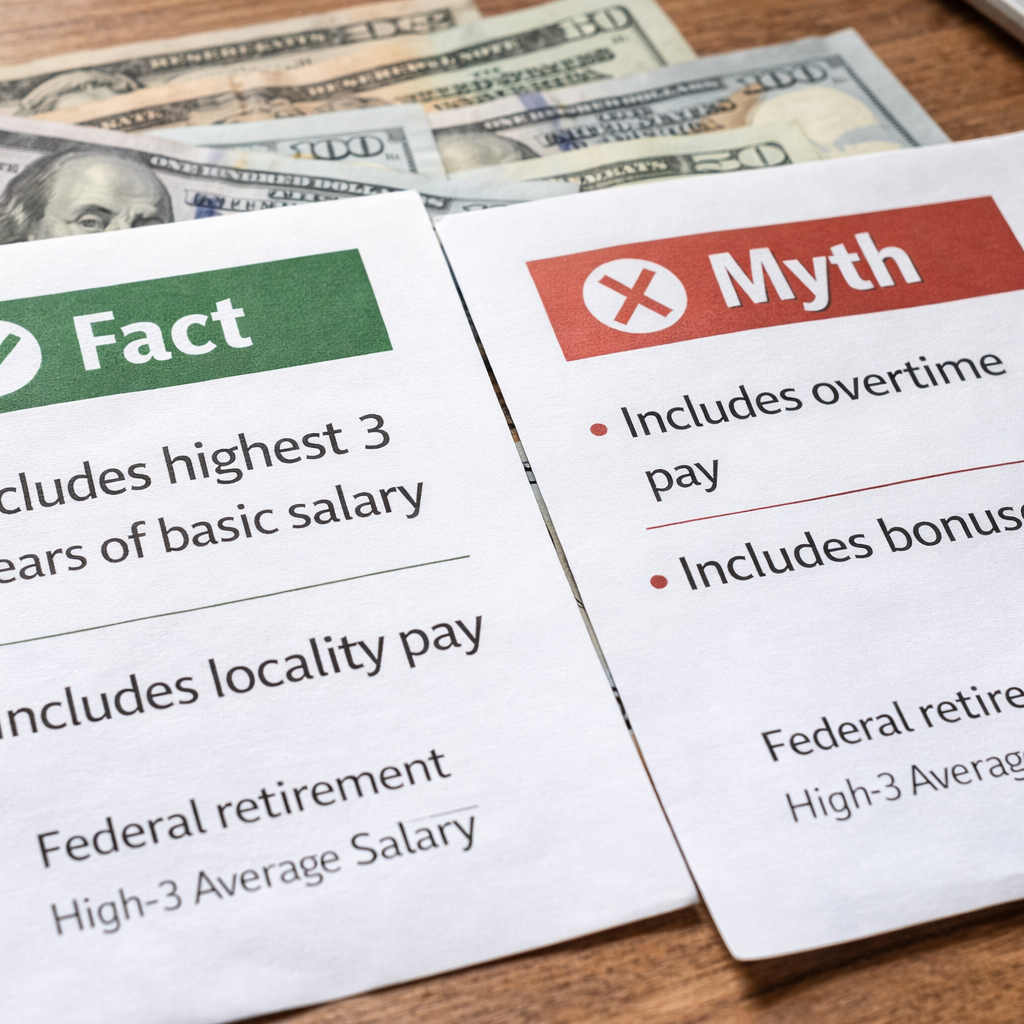

The Role of the High-3 Average in Retirement Calculations

Under the Federal Employees Retirement System (FERS), your pension is based on your “high-3″—the average of your highest three consecutive years of basic pay. For most employees, this includes:

-

Base pay

-

Locality pay (if applicable)

However, this could change. A 2025 legislative proposal seeks to exclude locality pay from high-3 calculations. If passed, this would directly reduce pension payouts for government employees who spent their careers in high-cost areas. While the bill is still under committee review, its potential impact is significant enough to merit your attention.

How Locality Pay Currently Impacts Your High-3

Currently, if you earn $120,000 in base pay and receive 25% in locality adjustments, your pension calculation would be based on $150,000. Excluding locality pay would instead drop that figure to $120,000, reducing your monthly annuity by hundreds of dollars.

Given that the average FERS annuity for 2025 is around $1,810 per month, even a small change in your high-3 can have long-term consequences.

Who Would Be Most Affected by the Change

The proposed exclusion of locality pay from pension calculations wouldn’t affect everyone equally. The impact would depend on several factors:

-

Geographic Location: Employees in high-cost areas with larger locality percentages would see the biggest reductions.

-

Proximity to Retirement: Those planning to retire within the next 1–3 years may not have time to adjust their pay structure or relocate.

-

Career Earnings History: If your high-3 years include heavy locality pay, your pension will be more vulnerable to the proposed changes.

-

Pay Structure: Certain specialized roles with different compensation components may see different impacts, depending on how their pay is structured.

This issue affects tens of thousands of employees, particularly those stationed in localities such as Washington, D.C., Los Angeles, and the Bay Area, where locality pay can exceed 30%.

Why the Government Is Considering the Change

The primary reason cited for the exclusion is cost containment. With increasing pension liabilities and pressures on the federal budget, lawmakers are looking for ways to reduce long-term retirement costs. Excluding locality pay from annuity formulas would achieve that—at the direct expense of employee retirement security.

Advocates argue that basic pay should reflect national standards, and any adjustments for local cost-of-living should only apply during active employment. Critics, on the other hand, say this undermines the value of locality pay and penalizes those who committed to long-term careers in expensive regions.

What You Can Do Right Now

Although the proposal is not yet law, there are proactive steps you can take now to minimize its impact if it is eventually passed:

1. Review Your High-3 Status

-

Obtain your earnings statement from your agency HR office.

-

Calculate whether your current high-3 years include high locality pay.

-

Consider whether a different assignment or position could increase your base pay.

2. Consult a Retirement Benefits Specialist

A licensed agent listed on this website can walk you through the specifics of your retirement portfolio and help you identify vulnerabilities. They may recommend accelerating your retirement, modifying your TSP allocations, or adjusting your retirement age.

3. Monitor Legislative Updates

Proposed changes to retirement benefit formulas often take months (or longer) to move through Congress. Stay informed through official channels or trusted retirement planning resources. Understanding where the legislation stands will help you make better-timed decisions.

4. Consider a Transfer or Promotion

If you are early in your high-3 period, a lateral move to a higher base-pay position (even in a lower locality pay area) could help offset the exclusion if it becomes law. The goal is to solidify your high-3 with strong base pay figures.

Implications for Your Long-Term Financial Planning

Even if the change doesn’t happen this year, it reflects a trend toward tighter scrutiny of retirement benefits. That alone is reason enough to take a closer look at your overall financial strategy.

Impact on Pension Income

Assuming a 30-year career, a 10% reduction in your high-3 average due to locality pay exclusion could lower your annual pension by thousands of dollars—adding up to a six-figure loss over your retirement.

Impact on Social Security and TSP Withdrawals

Because pension income is just one leg of the retirement stool (along with Social Security and the Thrift Savings Plan), you may need to draw more aggressively from TSP or delay Social Security to make up for lower annuity payments.

Reassess Your Retirement Timeline

If your retirement plans were based on assumptions about your pension that no longer apply, you may need to:

-

Postpone retirement by 1–3 years

-

Increase TSP contributions in 2025 and 2026 to build a larger cushion

-

Adjust withdrawal rates post-retirement to account for reduced income

How This Compares to CSRS Retirees

If you’re under the older Civil Service Retirement System (CSRS), you may not be affected the same way. CSRS pensions are calculated using a different formula and generally do not rely on locality pay in the same manner.

Still, if you’ve switched from CSRS to FERS or had hybrid service, it’s worth reviewing your eligibility breakdown. The proposed change targets FERS explicitly, but downstream effects could still emerge depending on how your years of service are split.

What Retirement Could Look Like If the Bill Passes

Let’s walk through what the future might look like under this proposal:

-

Employees who retire after January 1, 2026, may have their annuity calculated on base pay only.

-

Employees who retire before that date might be grandfathered into the old system, assuming no retroactive application.

-

Employees in the middle of their high-3 period may find their pension lowered even if they retire within a few years.

Again, none of this is finalized. But assuming a one-year implementation timeline from the date of passage, time is of the essence.

The Bigger Picture: What This Says About Retirement Policy in 2025

This potential change is part of a larger pattern. Over the last few years, retirement benefits for government employees have come under increasing scrutiny:

-

The average FEHB premium rose by 13.5% in 2025.

-

Legislative proposals have considered shifting to a voucher-style FEHB contribution model.

-

TSP G Fund returns have been debated in light of proposals to eliminate subsidies.

The exclusion of locality pay from pension calculations fits squarely within this trend. And while it may seem like a technical change, its ripple effects could be profound.

Protecting Your Retirement from Shifting Rules

It’s easy to become complacent when retirement benefits are managed by agencies and statutes. But in an environment where rules are subject to change, it’s more important than ever to stay engaged, review your plans annually, and adapt as needed.

You’ve put in years—sometimes decades—of service. You deserve to retire with the security you’ve earned. Don’t leave that up to chance.

Talk to a Retirement Professional Before the Rules Change

If you’re unsure how the exclusion of locality pay could impact your high-3 average and your pension, now is the time to act. Get in touch with a licensed agent on this website who can review your options and help you adapt your retirement plan to any upcoming changes.