Key Takeaways

-

The Postal Service Health Benefits (PSHB) Program in 2025 introduces major changes that every postal employee and retiree must understand to protect their healthcare and retirement benefits.

-

Decisions made today regarding Medicare, health coverage, and retirement timing could permanently affect your costs, coverage options, and eligibility for future benefits.

Understanding the Changing Landscape of Postal Employee Benefits

Postal employee benefits in 2025 are undergoing some of the most significant changes in decades. If you work for the Postal Service or are retired from it, you must be aware of new rules, tighter timelines, and higher stakes around your healthcare, retirement income, and overall financial future.

- Also Read: How-to Compare Inflation Protection Strategies for Federal Retirees in 2026

- Also Read: Health Expense Budgeting: 8 Tips for Retirees Planning Medical Costs

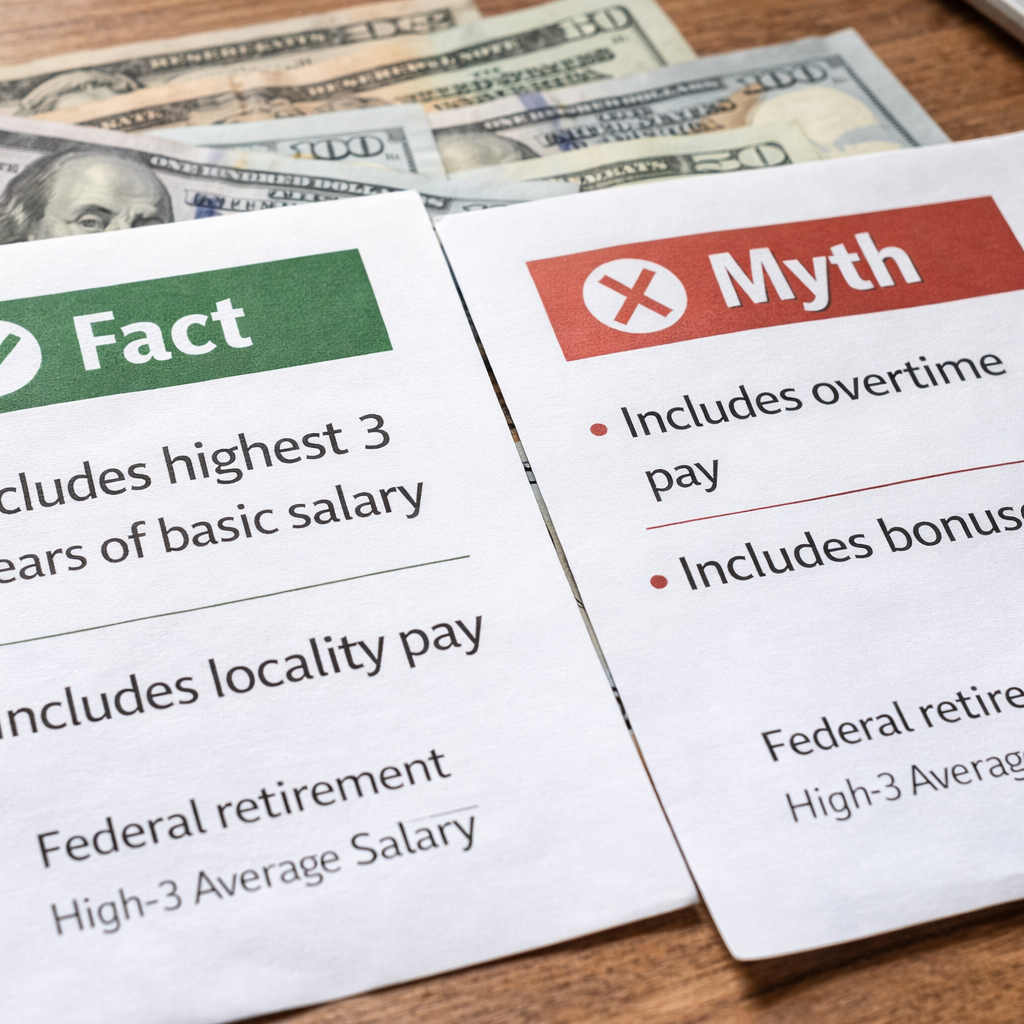

- Also Read: High-3 Average Salary Explained: Myths vs Facts for Federal Retirement

The Shift to PSHB: What It Means for You

The most sweeping change affecting postal employees this year is the replacement of the Federal Employees Health Benefits (FEHB) Program with the Postal Service Health Benefits (PSHB) Program.

-

Effective January 1, 2025, all postal employees and annuitants must be enrolled in a PSHB plan.

-

If you were previously covered under FEHB, you were automatically enrolled in a corresponding PSHB plan unless you made a change during the Open Season held from November to December 2024.

-

PSHB plans are designed to integrate more closely with Medicare Part B for eligible retirees and their family members.

Failing to meet Medicare enrollment requirements could now jeopardize your PSHB coverage after age 65, with limited chances to recover coverage later.

Medicare Enrollment Requirements: A New Mandatory Step for Many

Under PSHB rules in 2025, certain postal retirees and their covered family members must enroll in Medicare Part B when first eligible:

-

If you turned 64 or older before January 1, 2025, you may be exempt.

-

If you retired on or before January 1, 2025, you may also be exempt.

-

Otherwise, failure to enroll in Medicare Part B when first eligible could result in loss of PSHB health benefits.

You must be proactive during your Initial Enrollment Period around your 65th birthday, which spans 7 months (3 months before, the month of, and 3 months after turning 65). Missing this window may result in permanent late penalties and gaps in coverage.

Higher Out-of-Pocket Costs: Planning for Reality

2025 brings higher healthcare cost exposure for postal retirees and employees:

-

Deductibles in PSHB plans range between $350 and $2,000 depending on plan type and in-network or out-of-network care.

-

Out-of-pocket maximums reach $7,500 for Self Only and $15,000 for Self Plus One or Self and Family coverage.

While plans still offer robust coverage, the out-of-pocket expenses for major services or specialist care could create financial pressure if you are unprepared.

Coordinating your PSHB benefits with Medicare Parts A and B, when eligible, can significantly reduce deductibles, coinsurance, and copayment obligations.

Prescription Drug Coverage: Big Changes Under PSHB

As of 2025, postal retirees and family members eligible for Medicare are automatically enrolled in a Medicare Part D Employer Group Waiver Plan (EGWP) through their PSHB plan.

Key features include:

-

A $2,000 cap on annual out-of-pocket drug costs.

-

$35 monthly insulin limit for covered insulin products.

-

Expanded pharmacy networks.

Opting out of the Medicare Part D coverage embedded in your PSHB plan could cause you to lose drug coverage entirely, with limited ability to re-enroll later. Be cautious before declining.

Life Insurance, Dental, Vision: What Stays the Same

While PSHB changes healthcare, other core benefits for postal employees remain stable in 2025:

-

FEDVIP (Federal Employees Dental and Vision Insurance Program) still provides dental and vision insurance.

-

FEGLI (Federal Employees’ Group Life Insurance) remains available, although premiums increase with age.

-

Flexible Spending Accounts (FSAs) are still available for active employees, with a 2025 contribution limit of $3,300 for healthcare FSAs.

These programs have not transitioned to PSHB and continue separately.

Retirement Income: FERS Basics Stay, But Cost of Living Adjustments Matter More

Postal employees under the Federal Employees Retirement System (FERS) continue to receive:

-

A basic annuity based on their “High-3” salary average.

-

Social Security benefits.

-

Thrift Savings Plan (TSP) contributions.

However, the cost-of-living adjustment (COLA) for FERS retirees is reduced by 1% if inflation is under 2%. With 2025 seeing a moderate 2.5% COLA, retirees are receiving modest increases, but inflation risks remain a growing concern.

Careful TSP management, and possibly annuitizing part of your TSP balance, could help protect against inflation eroding your purchasing power.

Survivor Benefits: New Importance Under PSHB

Survivor benefits are critically important for maintaining health insurance after your death.

-

If you elect a survivor benefit when retiring under FERS, your eligible survivors can continue PSHB coverage.

-

If you do not elect a survivor benefit, your spouse and family lose eligibility for PSHB coverage after your death.

Given the higher costs and penalties for late Medicare enrollment, this protection is now even more valuable than in the past.

Timing Your Retirement: Why 2025 is a Pivotal Year

The transition to PSHB and Medicare integration makes 2025 a very strategic year to consider your retirement timing:

-

Retiring before age 65 but without planning for Medicare enrollment could leave you exposed.

-

Delaying retirement until after fully coordinating Medicare and PSHB benefits could save you thousands annually in health costs.

If you plan to retire in 2025, review your Medicare status carefully and consult with a professional before filing any paperwork.

Avoiding Pitfalls: Common Mistakes to Watch For

Postal employees and retirees should stay alert for these common mistakes:

-

Missing Medicare Part B enrollment deadlines.

-

Opting out of integrated Medicare Part D coverage.

-

Assuming PSHB automatically mirrors FEHB benefits exactly.

-

Failing to update survivor elections to protect future coverage.

-

Underestimating the value of TSP withdrawals during early retirement.

Careful annual reviews of your benefits—and your personal situation—are more necessary than ever.

Staying Proactive: How to Protect Your Benefits

To stay ahead of fast-moving changes, you should:

-

Track Open Season dates every year and review your PSHB plan.

-

Confirm Medicare eligibility status and enrollment obligations.

-

Evaluate TSP investments for income security and inflation protection.

-

Maintain updated life insurance and survivor elections.

-

Plan for higher healthcare costs when budgeting for retirement.

Postal employee benefits have become more dynamic and complex. Staying passive is no longer an option if you want to preserve your financial security.

Why You Need Trusted Advice More Than Ever

Given the intricate changes to PSHB, Medicare requirements, survivor protections, and retirement income planning, relying solely on outdated information or assumptions could be dangerous.

You are strongly encouraged to get in touch with a licensed professional listed on this website to receive personalized guidance based on your current status and future goals.

Getting expert advice now could prevent irreversible mistakes later.

Preparing for the Future of Postal Retirement Benefits

As 2025 unfolds, postal employees and retirees who adapt early to the PSHB transformation and Medicare coordination requirements will secure stronger healthcare coverage, lower costs, and better retirement security.

Do not wait until confusion or mistakes cost you valuable benefits. Be proactive, stay informed, and consult a licensed professional listed on this website for guidance tailored to your needs.