Key Takeaways

-

Planning early for your FERS retirement in 2025 helps you avoid benefit reductions and maximize income in retirement.

-

Coordinating your pension, Social Security, and TSP distributions strategically gives you more control over taxes and your long-term financial stability.

Understanding Your Eligibility Under FERS

If you’re thinking about retiring in 2025 under the Federal Employees Retirement System (FERS), your first step is confirming your eligibility. FERS allows for different retirement types, and each comes with its own set of requirements.

Immediate Retirement

You qualify for an immediate, unreduced annuity if:

-

You’re at least 62 with five years of service

- You’re at least 60 with 20 years

-

You reach your Minimum Retirement Age (MRA) with 30 years

In 2025, the MRA remains between age 55 and 57 depending on your birth year. Most FERS employees retiring now fall into the higher end of this range.

MRA+10 Option

If you have 10 or more years of service and have reached your MRA but don’t meet the age or service requirements for an immediate retirement, you can still retire under the MRA+10 provision. However, your annuity is permanently reduced unless you delay the start date.

Timing Your TSP Withdrawals Wisely

Your Thrift Savings Plan (TSP) is a major pillar of your FERS retirement income. When and how you begin withdrawing from it can affect your taxes, lifestyle, and portfolio longevity.

Required Minimum Distributions (RMDs)

As of 2025, RMDs begin the year you turn 73. That means if you turn 73 in 2025, your first RMD must be taken by April 1, 2026.

To make the most of your TSP, consider:

-

Withdrawing in low-tax years between retirement and age 73

-

Using partial withdrawals to manage tax brackets

-

Considering Roth conversions early on if you expect higher taxes later

Don’t Overlook the FERS Supplement

One often underutilized benefit is the FERS Special Retirement Supplement. If you retire before age 62 and qualify for an immediate unreduced annuity, you likely qualify for the supplement.

It bridges the gap between your retirement date and your Social Security eligibility at age 62. The supplement is calculated based on your years of FERS service and an estimate of your age-62 Social Security benefit.

However, it phases out entirely at age 62 and is subject to the Social Security earnings test if you continue working after retirement.

How FEHB Fits Into Your Retirement Picture

Your health benefits can continue into retirement if you:

-

Retire on an immediate annuity

-

Have been enrolled in FEHB for at least five consecutive years before retirement

In 2025, premiums under the Federal Employees Health Benefits (FEHB) Program have increased by an average of 11.2%. Retirees must pay the same share of premiums as active employees, but with no government payroll deduction, you’ll need to budget carefully.

If you’re eligible for Medicare at 65, coordinating your FEHB with Medicare Part A and Part B can significantly reduce your out-of-pocket expenses. Many plans offer reduced copayments and deductibles if you’re enrolled in both.

Consider Medicare Enrollment at 65

Even if you’re satisfied with FEHB alone, you should still consider enrolling in Medicare Part A when you turn 65 since it’s premium-free if you’ve paid Medicare taxes for at least 10 years.

As for Medicare Part B, you’ll want to weigh:

-

Your current FEHB plan’s cost-sharing with and without Medicare

-

Whether the added premium (projected at $185/month in 2025) is worth the reduction in out-of-pocket expenses

Failing to enroll in Part B when first eligible may result in late penalties unless you qualify for a Special Enrollment Period.

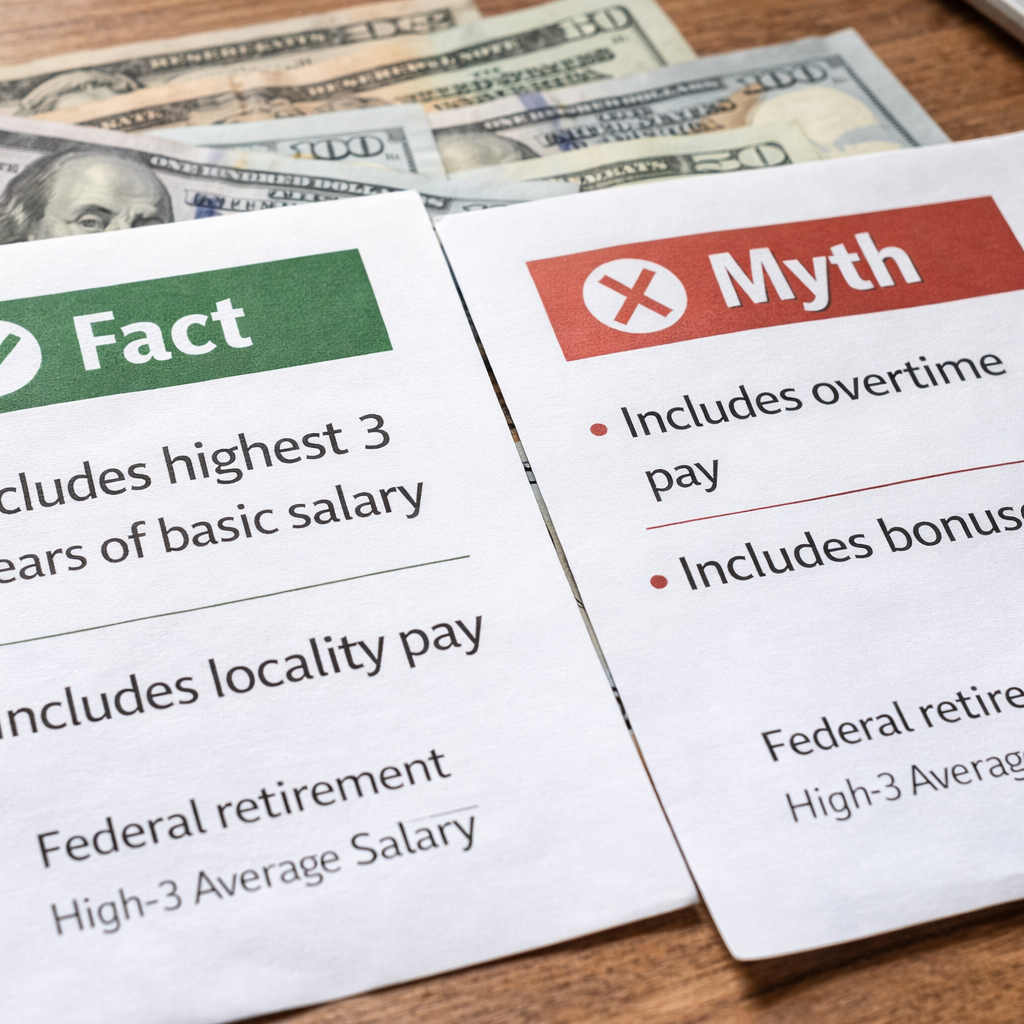

Know Your High-3 and the Impact of Locality Pay

Your FERS pension is based on your “high-3″—the average of your highest-paid three consecutive years. In 2025, legislative proposals have sought to remove locality pay from that calculation. While this hasn’t passed yet, staying informed is important because such changes could lower your annuity.

For now, locality pay is included, so if you’re in a high-cost area, this could significantly boost your pension calculation. If you’re considering transferring locations, it’s worth estimating the impact on your high-3.

Understand the Survivor Benefit Options

At retirement, you must choose whether to provide a survivor annuity for your spouse.

You have three choices:

-

Full survivor benefit (50% of your annuity)

-

Reduced benefit (25% of your annuity)

-

No benefit (spouse must sign consent form)

The cost of these options is deducted from your monthly pension. If your spouse will rely on your pension for future income, the full benefit provides peace of mind. Keep in mind, if you decline a survivor benefit, your spouse may lose access to FEHB coverage after your death.

Plan for Long-Term Care and Life Insurance

Many federal retirees keep basic FEGLI (Federal Employees’ Group Life Insurance) coverage. In 2025, premiums increase significantly with age, especially after age 65. It’s important to:

-

Review your coverage annually

-

Consider whether private life insurance or other financial products are more cost-effective

The Federal Long-Term Care Insurance Program (FLTCIP) is still suspended for new enrollees, but if you’re already enrolled, keep up with communications and evaluate whether the coverage still meets your needs.

Maximize Your TSP Contributions Now

If you’re still working in 2025, take advantage of higher contribution limits:

-

$23,500 elective deferral limit

-

$7,500 catch-up if you’re 50 or older

-

$11,250 catch-up if you’re between 60 and 63

These limits allow you to build tax-deferred savings quickly in your final working years. Review your TSP allocations to ensure your portfolio aligns with your retirement timeline.

Prepare for COLAs and Inflation

Your FERS annuity includes a cost-of-living adjustment (COLA), but it’s not full inflation protection unless you were under CSRS. FERS retirees only receive:

-

Full COLA if CPI is 2% or less

-

CPI minus 1% if CPI is between 2% and 3%

-

Capped COLA of 2% if CPI is above 3%

In 2025, the COLA is 3.2%. That means FERS retirees will receive a 2% COLA this year. Be sure to build inflation-resistant strategies into your income plan, such as TSP withdrawals and Social Security timing.

Create a Retirement Income Strategy

Combining your FERS pension, TSP, Social Security, and possible annuities or rental income requires thoughtful planning. You’ll want to:

-

Coordinate timing of income streams

-

Review tax implications annually

-

Use a retirement income planner or work with a financial advisor

The goal is to make your money last while supporting your lifestyle. Decisions you make now in 2025 can echo through the decades ahead.

Key Decisions Shape the Rest of Your Retirement

Retiring under FERS in 2025 comes with a wide range of options and responsibilities. From when to claim benefits to how to allocate your TSP, each decision can shape your financial outlook for years to come.

Take advantage of your remaining working months to:

-

Max out contributions

-

Evaluate healthcare options

-

Secure survivor and life insurance benefits

For guidance tailored to your circumstances, speak with a licensed agent listed on this website. Getting expert advice now can help you avoid common missteps and retire with confidence.