Key Takeaways

-

The FERS system is more than just a pension—it integrates multiple benefits, including Social Security and the Thrift Savings Plan, shaping your entire retirement outlook.

-

Understanding the full scope of FERS benefits can help you plan strategically for financial security, healthcare, and long-term income stability.

More Than a Pension: How FERS Defines Your Retirement Future

When you think about federal retirement, you probably picture a traditional pension. But the Federal Employees Retirement System (FERS) is far more than that. It’s a three-tiered system designed to provide financial security through multiple income streams, healthcare benefits, and long-term planning tools. If you’re a federal employee, understanding the full scope of FERS is crucial for making the most of your retirement years.

1. The Three Core Elements of FERS Work Together

- Also Read: How-to Compare Inflation Protection Strategies for Federal Retirees in 2026

- Also Read: Health Expense Budgeting: 8 Tips for Retirees Planning Medical Costs

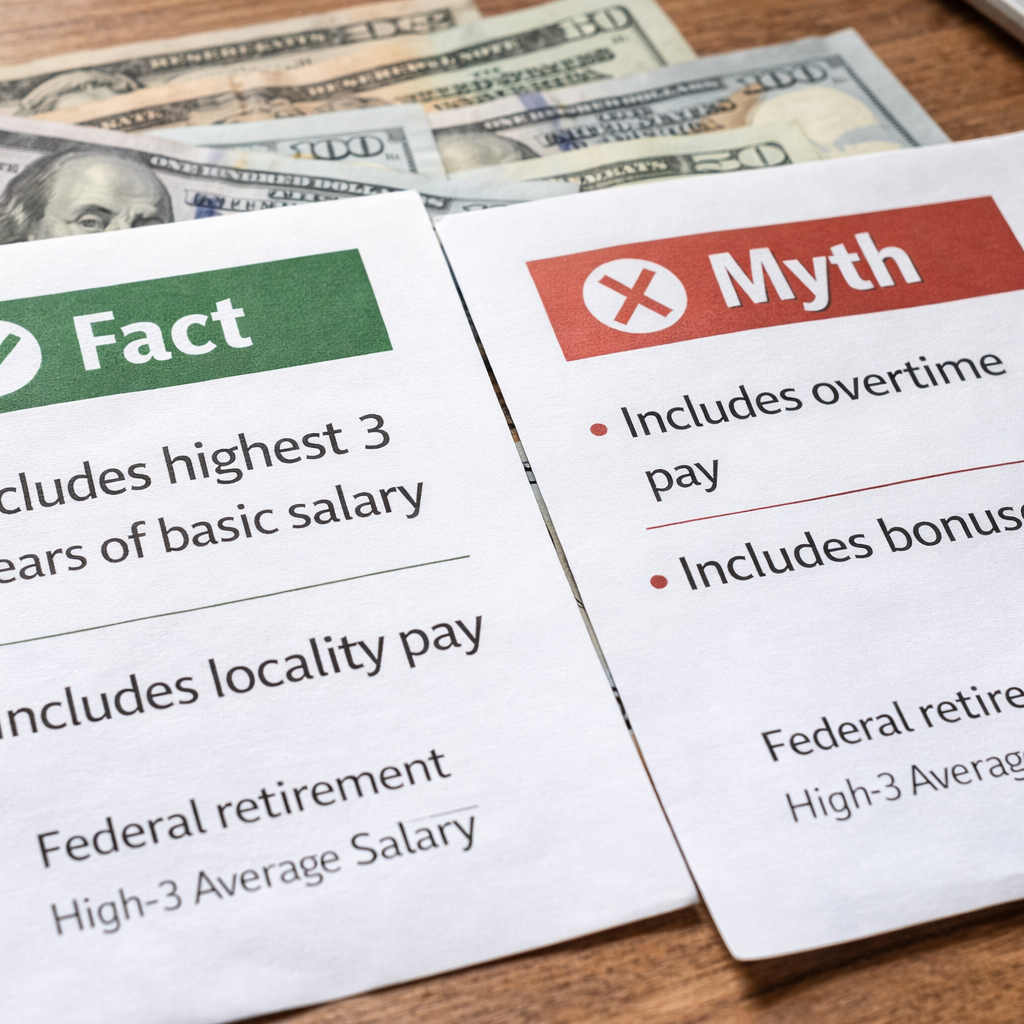

- Also Read: High-3 Average Salary Explained: Myths vs Facts for Federal Retirement

FERS isn’t just a single benefit; it’s a package that combines:

-

A pension (FERS Basic Benefit) — A defined benefit annuity based on your salary and years of service.

-

Social Security — Federal employees contribute to Social Security, adding another stream of income in retirement.

-

Thrift Savings Plan (TSP) — A retirement savings plan with government matching contributions.

Each of these components plays a distinct role in securing your financial future. Unlike private-sector employees who typically rely on Social Security and 401(k)s, federal workers have access to a more structured, multi-layered retirement system.

2. Your FERS Pension: A Reliable Income Stream

Your FERS Basic Benefit provides a guaranteed pension, but the exact amount depends on your High-3 Average Salary and years of service. The standard formula is:

1% of your High-3 salary x years of service (or 1.1% if you retire at 62 with at least 20 years of service).

This pension is lifelong and adjusted for inflation through Cost-of-Living Adjustments (COLAs). Unlike Social Security, which may fluctuate based on external economic factors, your FERS pension offers a predictable baseline of retirement income.

3. Social Security: The Second Layer of Your Retirement

One major difference between FERS and its predecessor, CSRS, is that FERS employees contribute to Social Security. This means you’ll be eligible for benefits starting at age 62 or later, depending on when you choose to claim them.

However, if you retire before age 62, you may be eligible for the FERS Special Retirement Supplement (SRS), which bridges the gap until Social Security kicks in. The SRS is particularly valuable for early retirees who want to maintain financial stability before reaching the official Social Security retirement age.

4. The TSP: Maximizing Your Investment Potential

The Thrift Savings Plan (TSP) is the third and often most overlooked pillar of FERS. This tax-advantaged investment account functions similarly to a 401(k), but with government matching contributions of up to 5%.

With contribution limits set at $23,500 in 2025 (plus additional catch-up contributions for those 50 and older), the TSP is a powerful tool for building wealth over time. Choosing the right mix of investment funds, including lifecycle funds that automatically adjust risk as you near retirement, can significantly impact your financial security.

5. Healthcare and Other Retirement Perks

Federal Employees Health Benefits (FEHB)

FERS retirees have access to FEHB coverage, which continues into retirement as long as you’ve been enrolled for at least 5 years before retiring. Unlike many private-sector retirees who lose employer-sponsored health benefits, federal retirees can maintain their healthcare, often with lower costs than private insurance options.

If you enroll in Medicare at 65, FEHB serves as supplemental coverage, reducing out-of-pocket expenses. This combination provides extensive healthcare security, making it one of the most valuable benefits of federal retirement.

Federal Employees’ Group Life Insurance (FEGLI)

If you have FEGLI, you can continue coverage into retirement, though costs increase with age. Evaluating whether to keep or reduce your FEGLI coverage is a crucial decision, especially as alternative life insurance options may become more cost-effective over time.

Long-Term Care Insurance

The Federal Long-Term Care Insurance Program (FLTCIP) is another option that helps cover extended care costs that Medicare and FEHB do not. This is particularly important for retirees concerned about nursing home care, assisted living, or home healthcare.

Planning Ahead: When and How to Retire Under FERS

Minimum Retirement Age (MRA) and FERS Early Retirement Options

Your Minimum Retirement Age (MRA) depends on your birth year, ranging from 55 to 57. You can retire under the MRA+10 rule (with a penalty) or with full benefits if you meet age and service requirements:

-

Age 60 with 20 years of service

-

Age 62 with 5 years of service

-

Any age with 30 years of service

Should You Take an Early Retirement?

If you retire early under MRA+10, your pension is reduced by 5% for every year under 62. However, federal employees in special categories (such as law enforcement) may qualify for early retirement without penalties.

How to Optimize Your FERS Retirement Strategy

To maximize your benefits, consider the following:

-

Max Out Your TSP Contributions: The government match is essentially free money, so contributing at least 5% is a must.

-

Time Your Retirement Wisely: Delaying retirement until at least age 62 increases your pension calculation and avoids penalties.

-

Review FEHB and Medicare Options: Coordinating these benefits properly can save thousands in healthcare costs over time.

-

Understand Your Survivor Benefit Options: If you’re married, deciding whether to elect a Survivor Benefit Annuity (SBA) is critical for your spouse’s financial security.

Making the Most of Your Federal Retirement

FERS offers one of the most comprehensive retirement packages available, but understanding how all the pieces fit together is key to financial success. Your pension, Social Security, TSP, and healthcare benefits all play a role in shaping your long-term security. By planning strategically, you can ensure that your retirement years are comfortable, financially stable, and well-prepared for any unexpected expenses.

If you need guidance on navigating your FERS benefits, get in touch with a licensed agent listed on this website who can help tailor your retirement strategy to your specific situation.