Key Takeaways

- Your High-3 salary directly shapes your federal retirement benefit, so understanding eligible earnings and counting periods is crucial.

- Factors like promotions, leave, and military service credit can influence your High-3 calculation and your future income.

If you’re close to retirement as a federal employee—or just planning ahead—you may be curious about the “High-3” salary calculation. This fundamental formula directly affects what you’ll receive in your federal retirement benefit. Let’s explore how your High-3 is determined and why it matters for your future.

What Is the High-3 Salary Rule?

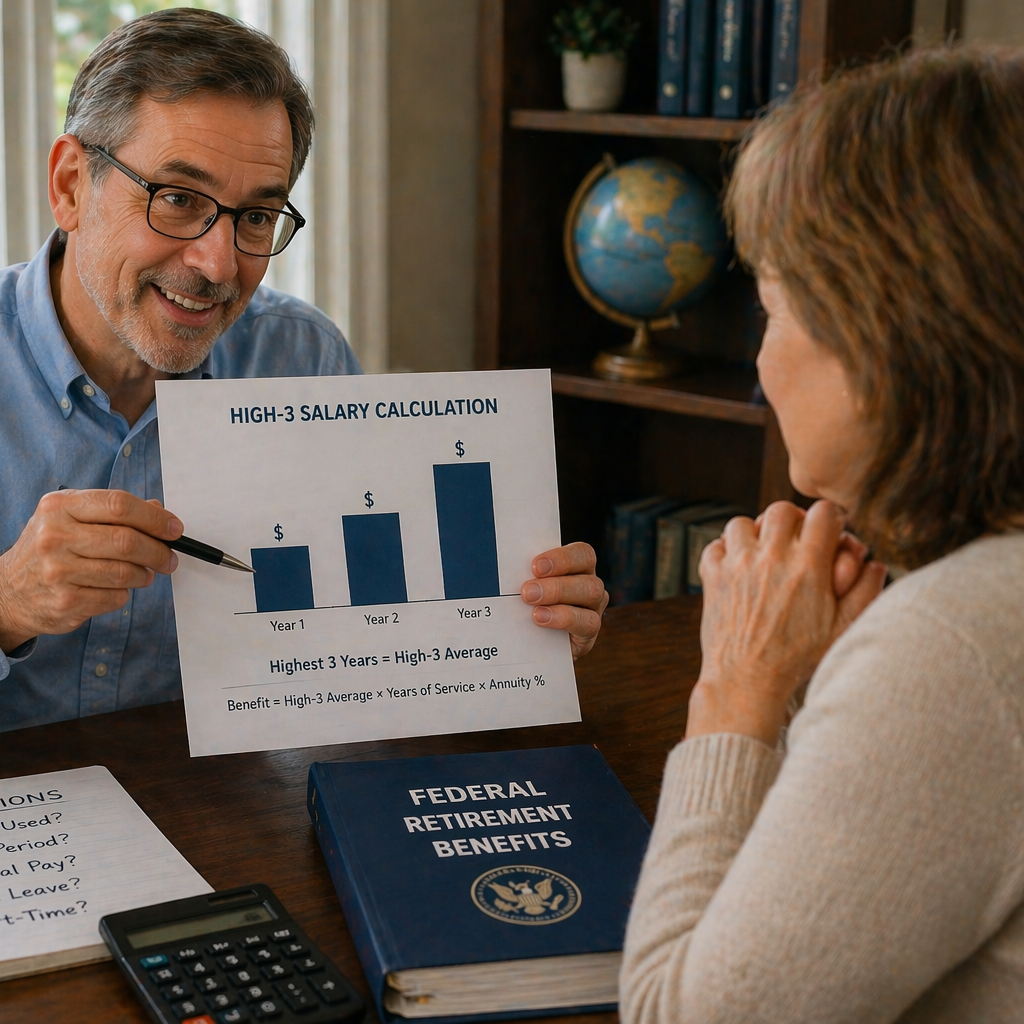

Definition of High-3 Salary

- Also Read: Special Category Employees & Military: Comparing FERS and Military Retirement

- Also Read: Survivor Annuity Options and Costs: Guide for Federal Retirees in 2026

- Also Read: Comparing HSA Rules and FSA Rules: Key Differences for Federal Retirees

Who Uses the High-3 Calculation

Most federal employees under the Civil Service Retirement System (CSRS) or the Federal Employees Retirement System (FERS) have their retirement annuity calculated using the High-3 rule. This approach ensures that your benefit is based on your most financially significant period of federal employment.

How Is the High-3 Salary Computed?

Understanding Eligible Earnings

When computing your High-3, only your basic pay counts. Basic pay includes your regular salary but not overtime, bonuses, awards, or other additional payments. Different federal jobs may have unique pay rules, but the principle remains the same: the calculation is rooted in your core salary.

Periods That Count Toward High-3

The High-3 period can be any span of 36 consecutive months during your federal career, not necessarily your final years. For some, it might be the last three years before retirement; for others, it could coincide with a long-term promotion or assignment when your salary peaked. Periods of unpaid leave may reduce your total countable months, so the right span is carefully determined from your service record.

Why Does the High-3 Formula Matter?

Impact on Federal Retirement Benefit

Your High-3 salary is the foundation of your federal retirement benefit. The government multiplies your High-3 by a formula (set by law) to establish your pension amount. A higher High-3 leads to a larger retirement benefit, driving the value of your lifelong income after federal service.

Factors Affecting Your Future Income

Because the High-3 is so influential, things like career promotions, pay raises, or long-term assignments can make a significant difference in your retirement outcome. Conversely, extended periods without pay or temporary moves to lower-salary roles may lower your High-3 and affect your post-retirement income.

What Factors Can Change High-3 Calculations?

Layoffs, Promotions, and Pay Changes

Career events such as promotions or reassignments can raise your salary, increasing your High-3 if the higher pay becomes part of a 36-month stretch. If you accept a position with lower pay, or your hours are reduced, that could lower your average. Layoffs don’t usually count against your High-3, unless a reduction in force changes your work schedule or base pay.

Leave Without Pay and Special Circumstances

Unpaid leave in excess of six months per year is not included in the retirement calculation, meaning it can break up what would otherwise be a high-earning period. Special assignments, temporary promotions, or periods of hazard pay need careful review, as not all extra compensation types count toward the High-3 average.

Are There Differences for CSRS and FERS?

Basic Comparison of Both Systems

CSRS and FERS are the two main retirement systems for federal employees. Both use the High-3 salary formula, but the benefit computations and eligibility requirements differ. CSRS generally applies to employees hired before 1984, while FERS covers most federal employees who joined after.

Implications for Benefit Calculations

Both systems use your High-3 years, but the percentage of your High-3 that forms your final benefit varies. FERS combines the annuity with Social Security and the Thrift Savings Plan, while CSRS offers a larger pension as a stand-alone benefit. Regardless of system, your High-3 period is always the foundation for the calculation.

What If You Have Military Service?

Military Service Credit in High-3

If you served in the military, those years may be credited toward your federal service under CSRS or FERS. Whether this time counts toward your High-3 depends on when and how you served, and whether you make a deposit to “buy back” your military service time.

Steps to Include Military Time

First, determine your eligibility to include military service. Next, submit the required documentation and, if necessary, make any required deposit. This process allows your military basic pay to count toward your High-3 average, potentially raising your retirement benefit.

How Can You Project Your Benefit?

Using Official Retirement Estimators

Federal agencies and various official online tools offer retirement estimators that use your actual or projected earnings record. These calculators let you experiment with different dates and salary histories to forecast your retirement benefit based on your High-3, but always use the most up-to-date and accurate information for planning purposes.

Reviewing Your Earnings Record

It’s important to check your personnel record regularly to confirm your salary history and verify which periods will count as your High-3. Corrections made before retirement are much easier than after, so stay proactive. Your agency’s human resources team can help you with record requests and understanding your specific situation.

Frequently Asked High-3 Questions

Common Myths and Clarifications

One common myth is that your High-3 must be the last three years before you retire—not true. It can be any three consecutive years with the highest average pay. Another misconception is that all pay counts toward High-3, but only basic pay is eligible. Knowledge is key to confident retirement planning.

Where to Find More Guidance

Federal human resources offices, official government websites, and retirement seminars provide a wealth of information on the High-3 calculation. When in doubt, turn to these sources for updates, FAQs, and step-by-step worksheets. Staying informed helps ensure a smoother transition to retirement.