Key Takeaways

-

A full FERS retirement package offers exclusive benefits that partial or early retirement options do not, including continued FEHB and enhanced annuity formulas.

-

Understanding all aspects of full FERS retirement helps you maximize long-term value, particularly in healthcare, cost-of-living adjustments, and survivor protections.

What Makes Full FERS Retirement So Valuable?

If you’re nearing retirement or already enjoying the benefits of federal service, understanding what comes with a full Federal Employees Retirement System (FERS) retirement package is essential. While early or deferred retirement paths offer flexibility, only full FERS retirement opens the door to specific protections and long-term financial advantages.

A full FERS retirement means you meet both the age and service requirements. As of 2025, the criteria are:

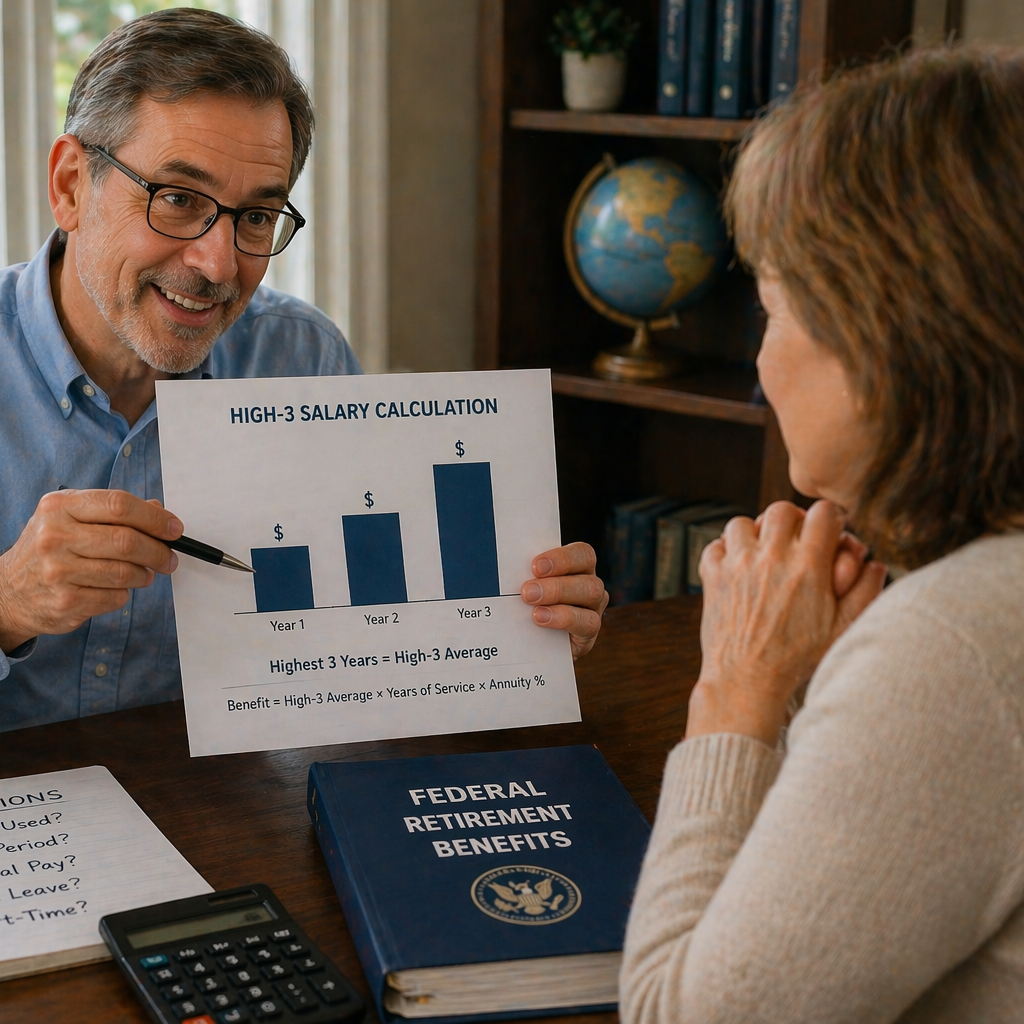

- Also Read: High-3 Salary Calculation Questions Answered in Detail: Understanding How Your Federal Retirement Benefit Is Determined

- Also Read: Understanding the Transition from FEHB to PSHB for Dependents: Eligibility, Coverage Options, and Critical Differences in Detail

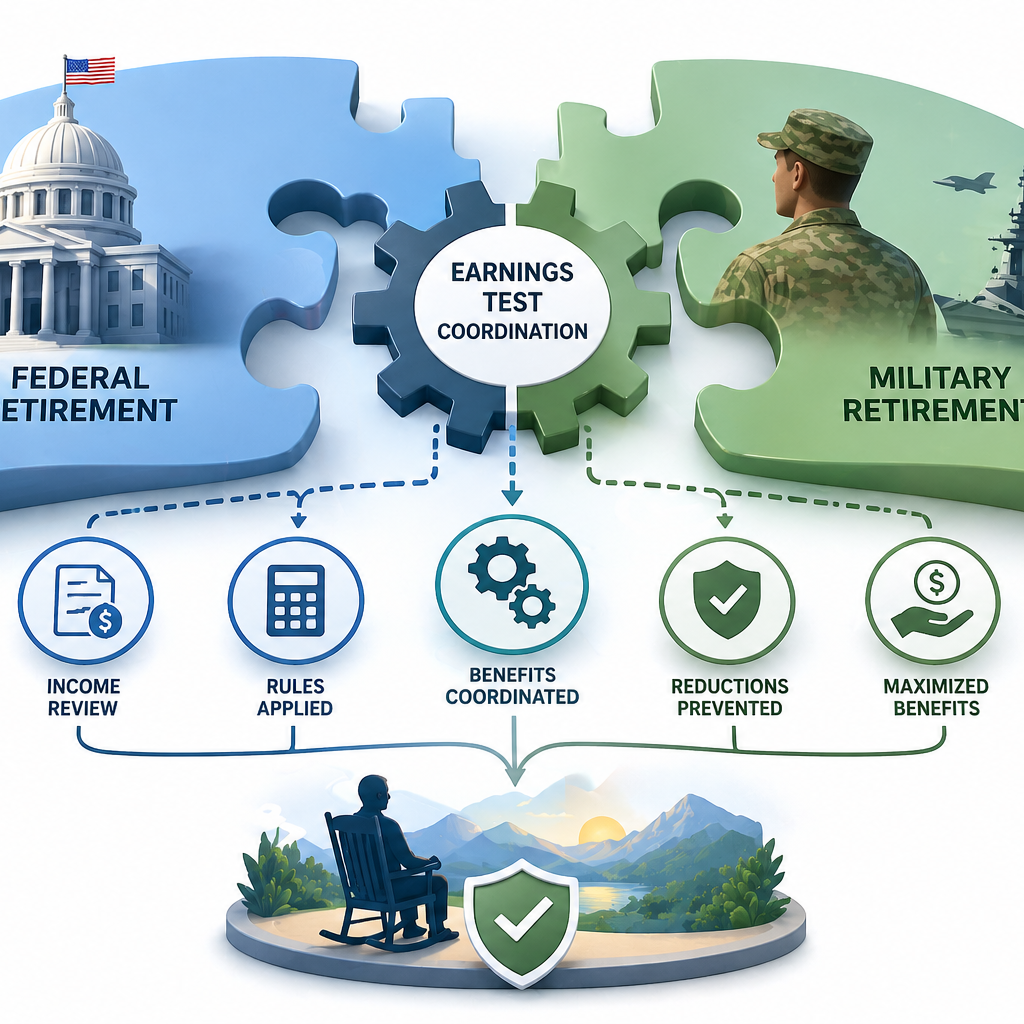

- Also Read: How Earnings Test Coordination Affects Federal and Military Retirement Benefits

-

Age 62 with at least 5 years of creditable service

-

Age 60 with at least 20 years

-

Minimum Retirement Age (MRA), between 55 and 57 depending on birth year, with at least 30 years of service

Meeting these thresholds unlocks several benefits that aren’t available otherwise.

1. Lifetime FEHB Coverage With Fewer Restrictions

One of the most valuable benefits of a full FERS retirement is lifelong access to the Federal Employees Health Benefits (FEHB) program. This is not guaranteed under deferred retirement options.

To continue FEHB into retirement, you must:

-

Be eligible for an immediate annuity

-

Be enrolled in FEHB for the 5 years preceding retirement (or since your first opportunity)

Full FERS retirement ensures these conditions are met. The government continues to pay about 70% of your premium, making it one of the most cost-effective health coverage options available to government retirees.

2. Cost-of-Living Adjustments (COLAs) on Your FERS Annuity

COLAs help your annuity keep pace with inflation. With full FERS retirement, you’re entitled to annual COLAs starting at age 62. Early retirees under MRA+10 or deferred options may miss out on COLAs until they reach the qualifying age.

In 2025, the COLA increase is 2.5%. These adjustments make a significant difference over a long retirement, particularly if you retire in your early 60s and expect 25 to 30 years of annuity payments.

3. Enhanced Annuity Formula With 20+ Years at Age 62

If you retire at age 62 or later with at least 20 years of service, your FERS annuity is calculated using a higher multiplier: 1.1% of your high-3 average salary per year of service, rather than the standard 1%.

This enhancement increases your lifetime income considerably. For instance, with a high-3 average of $80,000 and 30 years of service:

-

Standard rate: $80,000 x 1.0% x 30 = $24,000/year

-

Enhanced rate: $80,000 x 1.1% x 30 = $26,400/year

That difference grows with time, especially once COLAs are factored in.

4. Survivor Benefits Provide Ongoing Security

When you retire under full FERS, you can elect survivor benefits for your spouse. These benefits provide a portion of your annuity after your death, helping ensure financial stability for your loved ones.

The two main options are:

-

50% of your unreduced annuity

-

25% of your unreduced annuity

Choosing survivor benefits slightly reduces your monthly annuity during retirement, but it provides meaningful support after your passing. Without full FERS retirement, survivor benefits may be limited or unavailable.

5. Thrift Savings Plan (TSP) Withdrawal Flexibility

Upon full FERS retirement, you gain more options for accessing your TSP funds. You can:

-

Start Required Minimum Distributions (RMDs) at age 73

-

Set up installment payments, partial withdrawals, or full withdrawals

-

Roll over funds into other retirement accounts

While TSP is technically separate from FERS, full retirement gives you more freedom and fewer penalties. Early retirees or those who separate from service before the minimum age may face restrictions or early withdrawal penalties before age 59½.

6. Retiree Access to Federal Long Term Care Insurance

With full FERS retirement, you retain eligibility to continue existing enrollment in the Federal Long Term Care Insurance Program (FLTCIP). Although new enrollments are suspended as of 2025, existing policyholders can keep their coverage into retirement if they meet eligibility requirements.

Long-term care insurance can help cover expenses for in-home care, assisted living, or nursing facilities—critical costs that traditional insurance and Medicare may not fully cover.

7. Access to Retirement Counseling and Planning Resources

Employees retiring under full FERS often receive more thorough support from their agency’s HR and retirement planning offices. This includes:

-

Retirement seminars

-

Individual benefits counseling

-

Retirement estimate tools

This access helps you plan more precisely and avoid costly mistakes. Partial or deferred retirees may need to rely more heavily on outside assistance.

8. No Reduction for Early Retirement Penalties

One of the key features of a full FERS retirement is the absence of reductions that typically apply to early or deferred retirements. If you retire under MRA+10 with fewer than 30 years of service, your annuity may be permanently reduced by 5% for each year you’re under age 62.

Meeting the full retirement criteria removes these reductions entirely, preserving your full annuity value.

9. Inclusion in Federal Retiree Advocacy and Updates

Full FERS retirees continue to receive:

-

OPM newsletters and updates

-

Access to retiree groups and associations

-

Voting rights in certain retirement-related elections

Being part of this community can keep you informed about legislation, benefit changes, and advocacy efforts that affect your retirement income and healthcare.

10. Simpler Reemployment Rules If You Return to Government Work

If you decide to return to federal service after full retirement, the reemployment process is more transparent. Your annuity continues during part-time or temporary reemployment in most cases, although some salary offset rules may apply.

By contrast, deferred retirees returning to service face more complicated eligibility issues and may not regain certain benefits.

11. Continued FEDVIP Access for Dental and Vision

The Federal Employees Dental and Vision Insurance Program (FEDVIP) remains accessible in retirement if you retired with full FERS eligibility and had coverage prior to retirement. FEDVIP is not tied to FEHB eligibility but must be elected during open season or qualifying life events.

This continuity allows you to maintain comprehensive dental and vision coverage with group-rated costs and national access.

Why Full FERS Retirement Is More Than Just a Milestone

A full FERS retirement isn’t just about reaching a certain age or clocking in the required years. It’s about unlocking the full spectrum of benefits that protect your finances, health, and family for decades to come.

Making informed decisions about your retirement eligibility can shape your long-term financial picture. If you’re unsure about your retirement readiness, get in touch with a licensed agent listed on this website for professional advice tailored to your situation.