Key Takeaways

- Understanding the High-3 rule is essential for accurate retirement and pension planning as a federal employee.

- Reviewing your career timeline and benefit scenarios can help you maximize your federal retirement outcomes.

For federal employees, your retirement benefit depends on far more than simple years of service. The High-3 Salary rule plays a pivotal role in how your pension is calculated. By gaining clarity on how High-3 works, you can make more confident choices for your future.

What Is the High-3 Salary Rule?

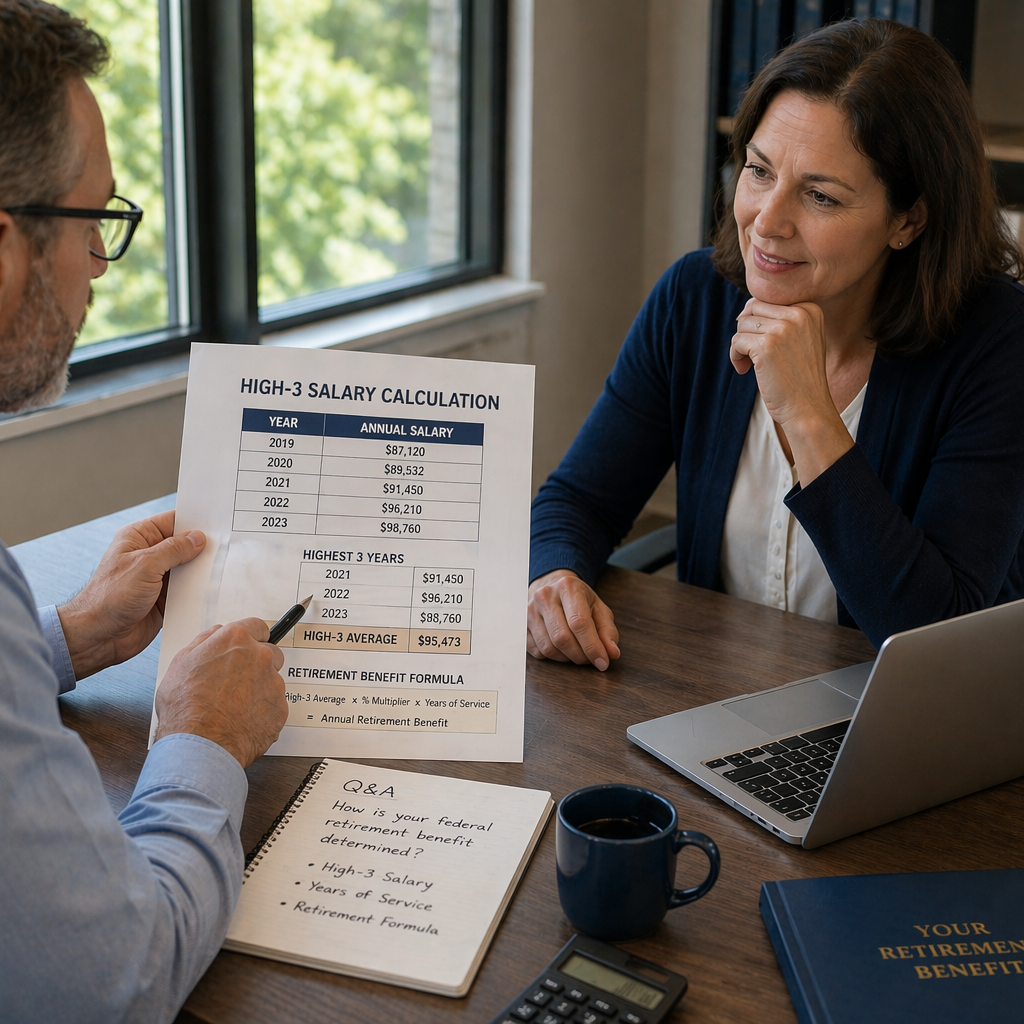

Definition of High-3 Salary

- Also Read: High-3 Salary Calculation Q&A Explained: How Your Federal Retirement Benefit Is Determined Step by Step

- Also Read: High-3 Estimator Worksheet Explained: Trends in Federal Retirement Benefit Planning and Calculation Strategies

- Also Read: How the Transition to PSHB Impacts FEHB Dependents: Eligibility, Coverage Options, and Critical Differences

Who Determines High-3 Calculation

Your federal agency’s human resources department works with official payroll records to determine your High-3 period. The calculations are based on your basic pay, as documented in your personnel and payroll data. While you can estimate your High-3 period and salary, the agency’s official records are the final source.

Which Earnings Are Included

High-3 strictly includes your regular basic pay. This means base salary, locality pay, and shift differentials if they’re part of your regular pay. It does not cover overtime pay, bonuses, awards, or other supplemental earnings. Accurate calculation relies on your position’s documented compensation during those three consecutive years.

How Does High-3 Affect Pensions?

Role in Pension Calculation

Your pension under both the Federal Employees Retirement System (FERS) and Civil Service Retirement System (CSRS) hinges heavily on your High-3 average. The formula multiplies your High-3 amount by specific accrual rates and your total years of service. This determines the monthly payment you’ll receive after retiring.

Importance for Retirement Planning

High-3 is one of the vital figures to understand and track as you move through your career. Because your pension will be calculated using this number, knowing when you’ve reached your highest earning period allows you to plan your retirement date strategically. For many, working a few more years at a higher pay grade can make a noticeable difference in future income.

Possible Impact on Future Benefits

A higher High-3 not only raises your basic pension amount but can also increase survivor benefits and cost-of-living adjustments (COLAs), since these features are often based on your pension size. However, since High-3 uses only consecutive years, sudden pay raises late in your career may have less impact if not sustained over three years.

What Are the Pros of High-3 Salary?

Predictable Income Calculation

One of the main advantages of the High-3 rule is that it provides a clear, predictable way to estimate your retirement income. Once you know your highest consecutive three years and your total creditable service, you can use federal resources to estimate your pension more confidently.

Potential for Higher Pension Amounts

If you advance into higher-paying positions or receive increased locality pay for several years, you can secure a higher High-3 period. This, in turn, can result in a greater pension than if your benefit was based on your entire career’s average pay, as seen in some non-federal pension plans.

Transparency in Benefit Formulas

Federal pension calculations are standardized and designed for fairness. The rules used for determining High-3 are applied equally across agencies, ensuring clear expectations. This transparency can help you plan and compare future scenarios as you think about career moves or retirement timing.

What Are the Cons of High-3 Salary?

Limited Inclusion of Overtime

While your base pay during your High-3 years is fully counted, any overtime, bonuses, or non-basic pay is left out. If you’ve had roles with frequent extra shifts or performance awards, these won’t boost your pension calculation in the way your regular pay can.

Possible Lower Payouts for Late Career Earners

If you receive a substantial pay jump in your final year or two of service, it may not fully benefit your High-3 calculation unless you sustain that higher salary for a consecutive three-year stretch. This can limit the impact of late-career promotions or moves to higher locality pay areas.

Challenges for Variable Income Roles

Jobs with fluctuating roles or assignments—such as those with temporary grade increases or special assignments—may find it harder to maximize High-3. Not all increases are reflected in your pension, which can make planning more complex for employees with non-traditional career paths.

Is High-3 Salary Right for You?

Reviewing Your Career Timeline

Take time to look back at your career. Identify when your basic pay was highest and whether those periods were consecutive. This exercise helps estimate your likely High-3 average and shows when a potential retirement might be most advantageous.

Assessing Pension Scenarios

Run multiple pension estimates, using online calculators and guidance from your human resources team. Evaluate how retiring earlier or later could affect your High-3, and what that means for your future income. Reviewing a few scenarios helps you understand your range of outcomes.

Questions to Discuss with Advisors

Consider talking to a federal retirement specialist or benefits counselor. Ask how your High-3 average is shaping up, when it could be highest, and what steps you can take to maximize this key figure. These conversations can clarify your planning and help set realistic expectations.

High-3 vs. Other Federal Benefit Calculations

High-3 Compared to High-5

Some non-federal pension plans use a “High-5” average, which means the average of your highest five consecutive years of pay. The High-3 calculation often leads to a higher base for most federal retirees, since it focuses on a shorter, peak-earning window.

Impact on Thrift Savings Plan (TSP)

Your High-3 salary does not affect contributions or matching rates in the Thrift Savings Plan (TSP), which is your retirement savings account. However, your basic pay during that period can influence how much you choose to contribute. The pension and TSP function independently, but together they create a broader retirement strategy.

Other Federal Retirement Metrics

Aside from High-3, other elements that matter in your retirement calculations include total years of service, age at retirement, and choices about survivor benefits or Social Security integration. Familiarizing yourself with all the factors empowers you to make the best decisions for your personal goals.