Key Takeaways

- Enrolling in Medicare impacts your ability to contribute to an HSA, making careful timing critical.

- Federal retirees should evaluate employment status and healthcare priorities before choosing when to enroll in Medicare.

Understanding how Health Savings Accounts (HSAs) and Medicare interact is a vital step for federal retirees planning their healthcare. Timing your decisions can affect both your insurance coverage and your financial flexibility in retirement. Let’s break down how these programs work together, what to consider, and review a practical case study to help guide your choices.

What Are HSAs and Medicare?

Health Savings Accounts Overview

An HSA is a special, tax-advantaged account used to pay for qualified medical expenses

- Also Read: Special Category Employees & Military: Comparing FERS and Military Retirement

- Also Read: Survivor Annuity Options and Costs: Guide for Federal Retirees in 2026

- Also Read: Comparing HSA Rules and FSA Rules: Key Differences for Federal Retirees

Basics of Medicare for Retirees

Medicare is a federal health insurance program for individuals age 65 and older or with certain disabilities. It has several parts: Part A (hospital insurance), Part B (medical insurance), and Part D (prescription drug coverage), among others. Federal retirees often pair Medicare coverage with their Federal Employees Health Benefits (FEHB) plan to have broader protection as they age.

How Do HSAs Interact With Medicare?

Eligibility Rules for HSAs

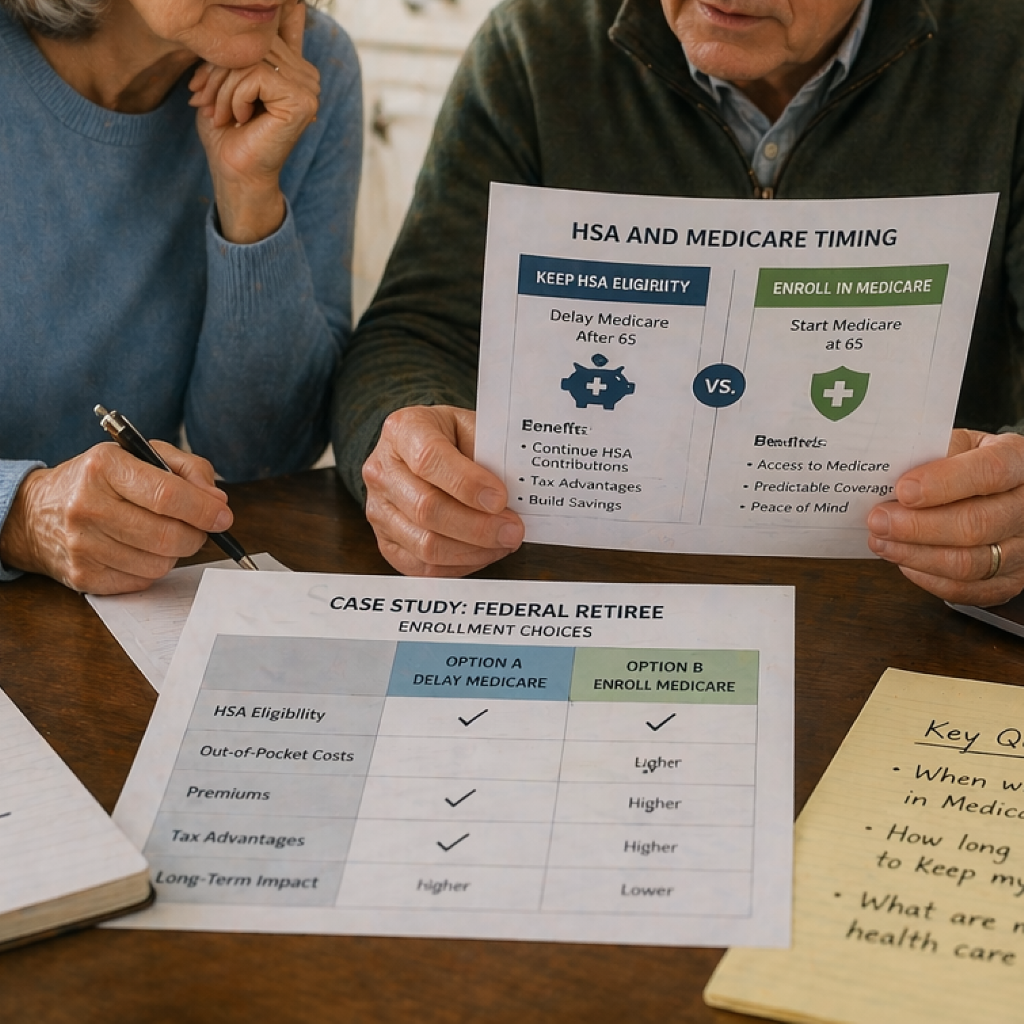

You’re eligible to contribute to an HSA only if you’re enrolled in a qualifying high-deductible health plan and not enrolled in any other health coverage, including Medicare. Once you are covered by any part of Medicare, you can no longer contribute new funds to your HSA. However, your existing HSA savings remain available for use on qualified medical expenses.

Impacts of Medicare Enrollment on HSAs

Enrolling in Medicare changes your HSA eligibility. Medicare coverage—whether you sign up for Part A, Part B, or both—means you must stop contributing to your HSA as of your effective enrollment date. Importantly, Medicare Part A often enrolls retroactively up to six months if you delay signing up past age 65, which can cause unexpected tax penalties if you continue making HSA contributions during that period. Carefully tracking your enrollment timing is vital to avoid issues.

When Should Federal Retirees Enroll in Medicare?

Typical Enrollment Periods

For most people, Medicare enrollment happens around your 65th birthday. The “Initial Enrollment Period” spans seven months—three months before, the month of, and three months after you turn 65. Federal retirees who are still working and covered by FEHB through active employment may choose to delay enrolling in Part B without penalty, but Part A is often automatic.

What Happens if You Delay?

If you wait to enroll in Medicare after your 65th birthday and you do not have job-based insurance through active employment, you could face higher premiums due to late enrollment penalties. On the other hand, if you keep working and maintain employer coverage, you may be able to delay Part B without a penalty. However, be aware that once you enroll in Medicare, even retroactively, you must stop your HSA contributions immediately.

Case Study: Timing Enrollment Choices

Background and Scenario Details

Consider a federal retiree named Linda who turns 65 but continues to work part-time for the federal government. She has FEHB and an HSA-qualified high-deductible health plan. Linda wants to maximize her HSA savings while ensuring she doesn’t miss critical Medicare deadlines or risk penalties.

Decision Factors Analyzed

Linda weighs several key issues:

- HSA Contributions: If she enrolls in any part of Medicare, her HSA eligibility ends. Delaying both Part A and Part B allows continued HSA contributions, but only if her employer coverage meets federal requirements.

- Medicare Enrollment: If Linda delays Medicare, she should stop HSA contributions at least six months before she plans to enroll, due to potential retroactive Part A coverage. If she needs the higher HSA balance, early planning helps avoid tax concerns.

- FEHB Coverage: FEHB may remain her primary coverage until she stops working. Coordinating Medicare and FEHB can provide strong retirement healthcare, but must be timed carefully with HSA rules.

What Factors Affect Enrollment Decisions?

Employment Status Considerations

Whether you are still working (and eligible for FEHB through active employment) directly impacts your options. If you’re employed by the federal government or another employer with a group health plan, you may be able to delay Medicare Part B without penalty. This choice preserves your ability to contribute to an HSA, provided you remain in an eligible health plan.

Coverage Needs and Healthcare Costs

Your expected healthcare needs shape your decision. If preserving your HSA is a top priority—perhaps to save for future medical expenses—delaying Medicare enrollment may make sense. But if you need the comprehensive coverage Medicare and FEHB together provide, early enrollment may be more valuable. Comparing coverage details and out-of-pocket costs is vital as you plan.

What Are Common Misconceptions?

HSA Contributions Versus Medicare

A frequent misunderstanding is that you can keep adding to your HSA after enrolling in Medicare. In reality, Medicare enrollment—whether just Part A or any part—disqualifies you from new HSA contributions. Only previous funds can be used, not new deposits.

Timing Myths and Clarifications

Another myth is that delaying Medicare automatically leads to penalties. In truth, as long as you have qualifying health coverage through current employment, you can postpone Part B without extra costs. However, it’s crucial to understand the interplay between enrollment dates and HSA eligibility to avoid surprises.